Bitcoin: Litman Gregory Research Review

This may come as no surprise to investors who know us, but we would be very cautious about buying cryptocurrencies. We are nowhere close to owning them in our client portfolios. There are three broad elements to our skepticism and caution toward bitcoin as an investment.

1. The Underlying Fundamentals & Risks

There is no way we know of to value bitcoin on a fundamental basis. What is its fair value? There are no cash flows or yield associated with bitcoin. That creates a huge hurdle for us to incorporate it into our investment approach, which is first and foremost based on understanding the economic fundamentals and market valuations of each asset class we may own and how the asset is likely to perform in different macroeconomic scenarios.

Turning to the risks, they are numerous and significant, in our view. We’d start with the existential regulatory risk. The Bank Credit Analyst recently wrote about this, arguing: “Bitcoin’s ability to facilitate anonymous transactions is also its Achilles heel. The widespread use of bitcoin would make it more difficult for governments to tax their citizens.” As a result, “Governments will step in to ban or greatly curtail bitcoin’s usage” before it reaches a critical mass as a viable medium of exchange. And as a result, bitcoin’s utility as a “store of value” will disappear.

Just last week, both the United Kingdom’s Financial Conduct Authority and the European Central Bank highlighted the need for more stringent regulatory scrutiny of cryptocurrencies, noting the criminal activity often associated with it.

Bitcoin and other cryptocurrencies also face competitive risks, technological risks, fraud, and market manipulation risks.

Based on our current understanding, there are reasonable scenarios where the price of bitcoin, at some point, could go to zero. As a rule, we don’t tend to favor investments that have zero as their downside.

2. Bitcoin’s Price Performance Profile

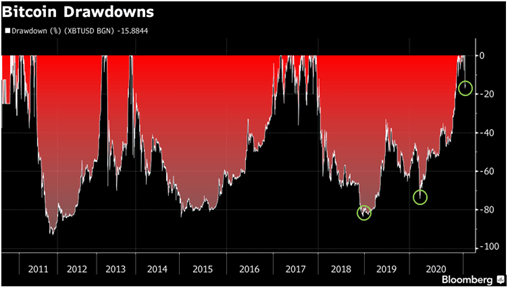

Bitcoin in a word is volatile—extremely volatile—on a day-to-day basis. And it has had massive drawdowns. The chart below tells the story. To mention a few highlights:

- It declined 83% from late 2017 to 2018.

- In February and March last year, it fell over 50%.

- And in January 2021, it dropped 27% in two days from its intra-day high on Friday, January 8, to its intra-day low on Monday, January 11.

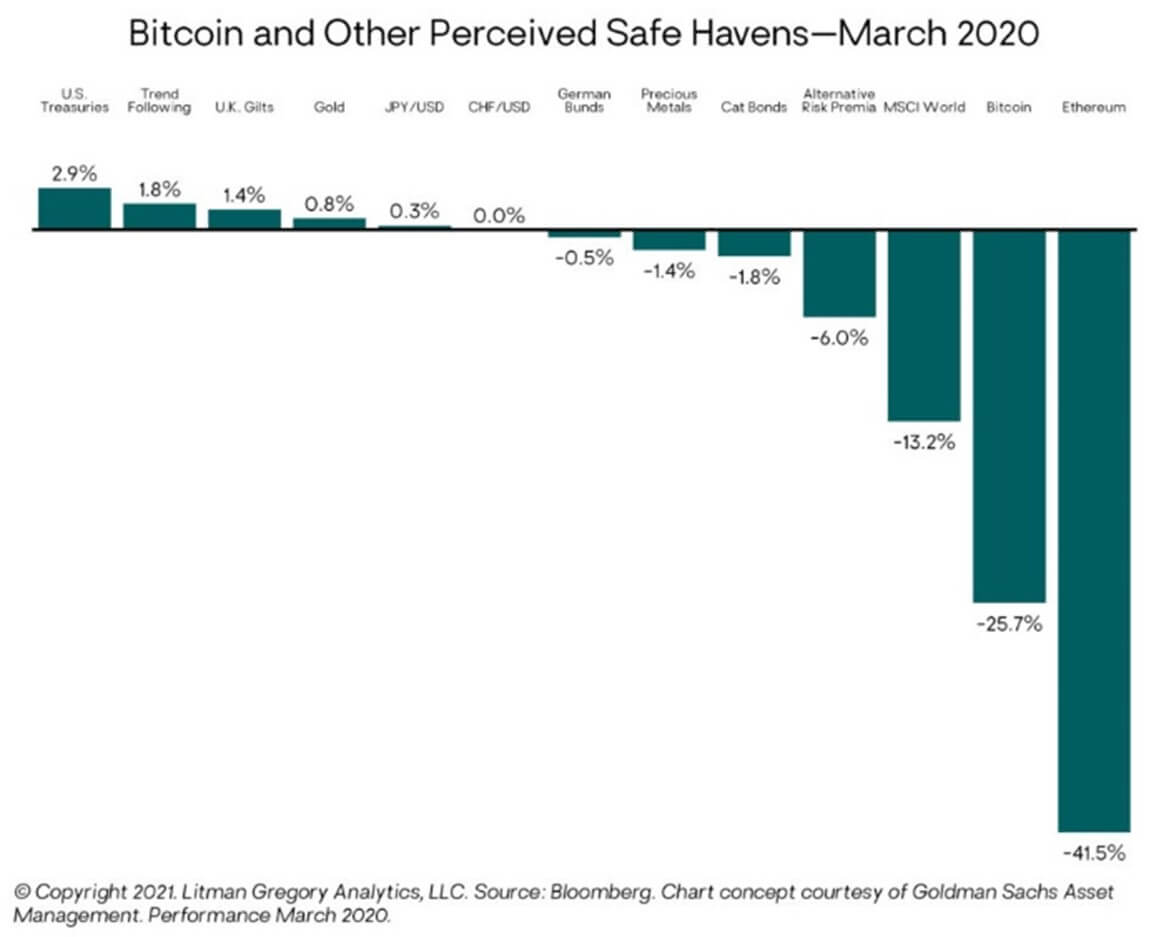

Bitcoin also hasn’t been a consistently good hedge against market shocks or equity bear markets. As the chart below shows, it lost 26% in March 2020 while global stocks dropped 13%. Meanwhile, gold was up 0.8% and U.S. Treasury bonds gained nearly 3%. Even better, our managed futures funds were up 6% to 8%.

So, bitcoin has been behaving more like a speculative “risk-on” asset—correlated with other risk assets like stocks—than a defensive portfolio diversifier.

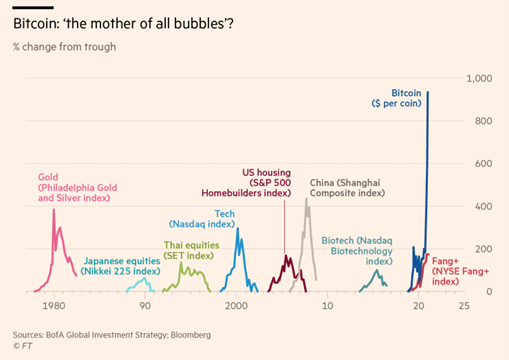

And many commentators are pointing to its stratospheric rise last year as evidence it is in a bubble.

3. The Behavioral Aspects

And that brings us to the behavioral aspects of owning bitcoin. Given its extremely high volatility without an underlying fundamental or valuation-based foundation, it is likely to be an extremely difficult investment for most people to stick with. The potential for getting whipsawed—buying high and then selling low—is extreme with such a volatile and non-fundamentally-driven asset.

A Speculation, Not an Investment

So, to sum up, our view hasn’t changed from what we wrote three years ago, just as bitcoin was hitting what turned out to be a peak in the frenzy of December 2017. And that is: Buying bitcoin is not investing, it’s speculating.

And speculating can be a fun game for some people with some small portion of their money. But we aren’t hired to speculate with the assets our clients have entrusted to us. And we don’t need to own bitcoin or play the cryptocurrency game to achieve our client’s investment goals.

—Jeremy DeGroot, CFA (1/29/21)