Expectations for the Economy Post-Election

In the leadup to the U.S. Presidential election, investors faced uncertainty about the outcome, which led to stock market volatility and declines in October. Post election, investors reacted positively to the end of that uncertainty and their focus shifted to assessing what the longer-term impacts of a Trump presidency may be.

With a Trump presidency, expectations are for less regulation and lower taxes. At the same time, there are now more questions around the economic impact from talks of tariffs and mass deportations. With republicans in control of the Senate and the House of Representatives, there is higher likelihood now of Trump proposals being enacted.

Among the issues of interest, one topic most seemed to agree on is that deficit spending would continue. An estimate from the Committee for a Responsible Federal Budget estimated that national debt would increase by $4 to $8 trillion over the next 10 years. The concern with an increasing deficit is that it necessitates more debt issuance, which can lead to higher interest rates, resulting in a risk to economic growth. (Whatever impact may be realized from the Department of Government Efficiency, or DOGE, remains to be seen in terms of its ultimate materiality.)

With the expectation of steadily increasing budget and trade deficits, combined with geopolitical tensions, questions remain about the long-term impact on the U.S. dollar and how that could impact the U.S. economy.

The U.S. Dollar

Headlines are increasingly about the risk of “de-dollarization,” or the movement away from using the U.S. dollar as the main currency of exchange. The concern is that this trend will ultimately send the value of the dollar sharply lower.

Supporting this concern are rising geopolitical and trade tensions, which have understandably increased some foreign countries’ anxiety about holding significant reserves in dollar-based assets. Examples include the tensions between the U.S. and China, and the economic sanctions imposed on Russia—the freezing of reserve assets— following their conflict with Ukraine. We have also seen news that China started using the yuan in commodity trades with partners such as Argentina and Brazil and they are exploring a common non-dollar currency.

Indeed, there is evidence of global diversification away from the U.S. dollar, but we think the factors supporting the dollar’s dominance remain entrenched, and any meaningful de-dollarization will likely take decades. China, specifically, has been working on diversifying their reserves for over a decade and data shows that China has indeed been selling their U.S. Treasury holdings. During that time, markets have worried about what would happen if China sold all their U.S. Treasury holdings. However, recent work by Brad Setser, a former Treasury official and fellow at the Council on Foreign Relations, shows that the percentage of China’s reserves in dollar bonds has remained stable at around 50% since 2015.

Setser points out that China has been shifting Treasury holdings that show up in official U.S. data to offshore custodians and into other dollar-based assets, such as agency bonds. This is not to say that China doesn’t have ambitions to “de-dollarize” their economy. But for now, China’s selling of U.S. Treasuries seems to be more an exercise of diversification of their dollar assets, rather than full divestiture.

The U.S. dollar remains the world’s primary reserve currency and is by far the most used currency for transactions around the world. The majority of global trade is done in U.S. dollars—even when the U.S. is not part of the transaction. Analysis from the Brookings Institute shows that 54% of global trade invoices are done in dollars and 88% of foreign exchange transactions happen in dollars. The lack of a viable alternative has helped the U.S. dollar remain dominant.

The euro and Chinese renminbi are the first two currencies that are often held up as alternatives to the dollar. However, for now, Europe’s less-liquid markets, decreasing economic strength, and political dysfunction make it hard to see it dethroning the dollar. The renminbi is also illiquid compared to the dollar, and it is still effectively pegged to the dollar and China’s strict capital controls make it difficult to move money in and out of the country. Other currencies could, at the margin, challenge the U.S. dollar should the U.S. continue to exert unwelcome influence through its control of the dollar. As mentioned above, taking the top spot from the dollar seems unlikely in the near term and any meaningful transition would take decades.

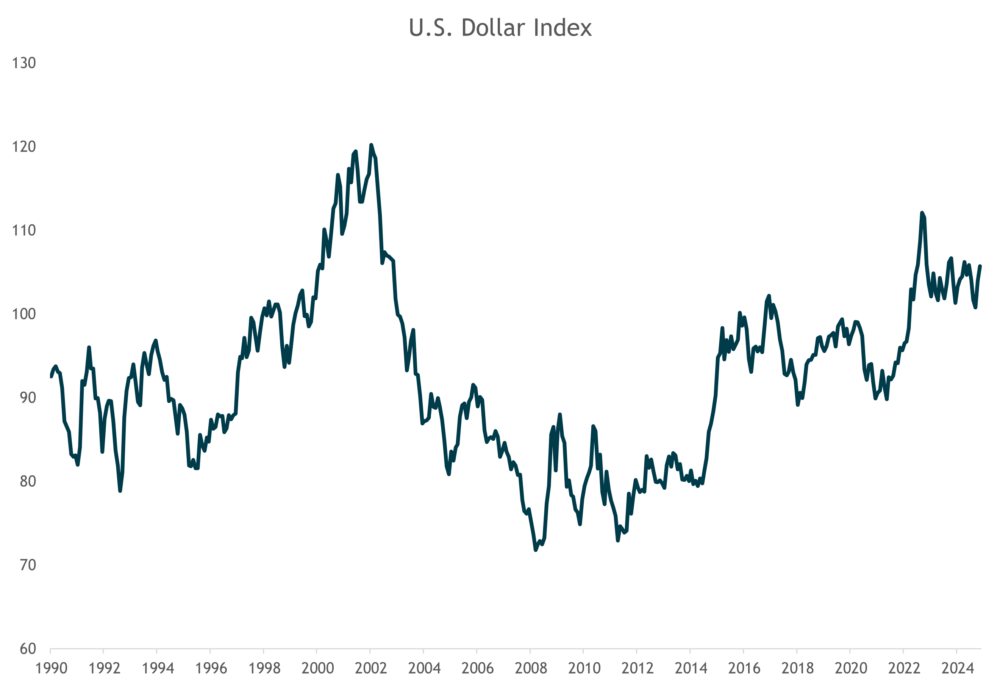

From a valuation perspective, the dollar has appreciated significantly since the Great Financial Crisis in 2008. This has been a headwind to returns for unhedged foreign assets. Since the start of 2010, the U.S. dollar index has gone from roughly 78 to over 106 today—more than a two-thirds increase (see chart below). The past couple years has seen the dollar trade sideways in a range from 100 to 105. Whether it definitively breaks out of that range following the U.S. election remains to be seen. However, should the dollar find a new trend, the shorter-term momentum would appear to favor the upside for several reasons.

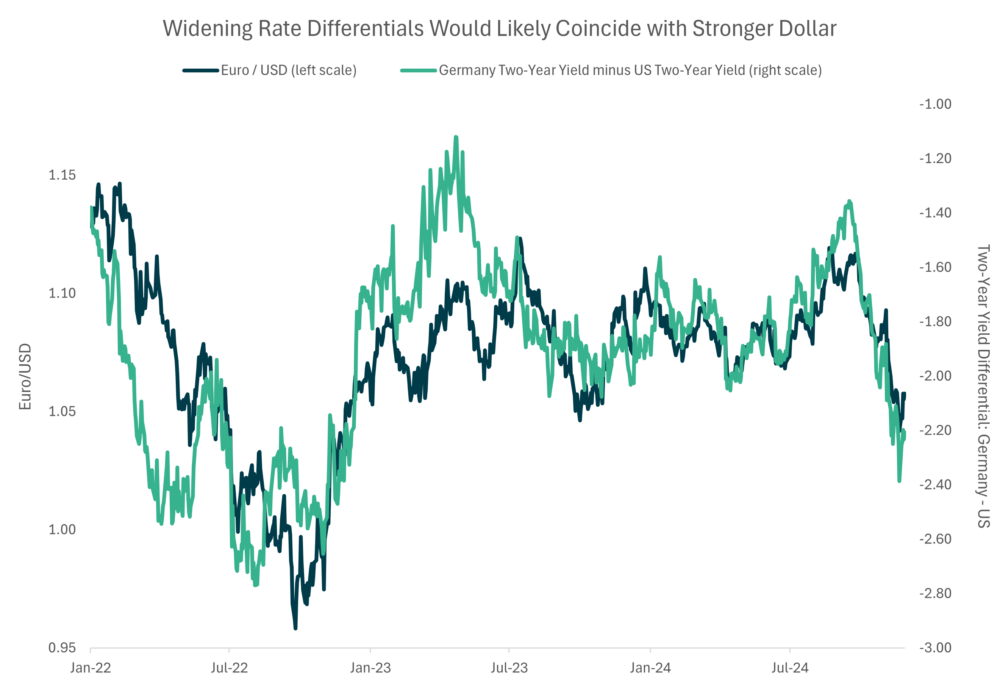

First, economic growth in the U.S. remains persistent whereas it continues to prove challenging in China and Europe. For example, Europe’s largest economy, Germany, has seen its economic growth stagnate for the better part of two years. Relative weakness in Europe could mean they cut interest rates meaningfully in 2025, whereas the U.S. might be forced to keep rates higher amid persistent growth. Relatively higher U.S. rates due to widening growth expectations could mean more demand for the dollar.

Second, other factors could benefit the dollar next year including some of President-elect Trump’s policies, such as tax cuts and deregulation. Both would be tailwinds for the dollar, but of course it remains to be seen what gets implemented. Trump’s Treasury Secretary pick, Scott Bessent, has promoted a “3-3-3” policy (3% federal deficit, 3% GDP growth, produce 3 million more barrels of oil daily) which would be dollar positive as well.

Third, tariffs on trading partners would depreciate their currencies and strengthen the dollar further. Any ratcheting up of trade tensions would likely bring more upside to the dollar.

One scenario that could hurt the dollar next year would be a sharp acceleration of economic growth outside the U.S. But for now, growth in the U.S. is increasing at a faster pace than other countries, particularly the euro zone, where growth has slowed. Longer term, there are reasons to expect a lower dollar—namely the U.S.’s twin deficits (combined trade and budget deficits). Policies that would further widen the twin deficits would deteriorate the dollar’s standing.

Despite what could be a longer-term issue for the dollar, we see more reasons why the dollar could be supported at these levels in the short term. If a recession in the U.S. does occur, then the dollar will benefit from its counter-cyclical, safe-haven properties. If a U.S. recession doesn’t come to pass, bond yields will likely remain elevated, also supporting the dollar. For now, we see dollar strength persisting due to continued entrenched advantages enjoyed by the U.S.

U.S. Dollar Exposure in Portfolios

For now, we remain cautiously optimistic about the current investment landscape. We remain at our globally diversified long-term strategic allocations for equities – which provides some hedge to the U.S. dollar from international positions. Within fixed-income, we continue to focus on less interest-rate sensitive bonds, specifically shorter-term maturities with higher yields. We think this fixed-income positioning will provide portfolios with a smoother ride and better risk-adjusted returns.

While there are promising signs of growth and resilience in the economy, and reason to believe the U.S. dollar will hold its strong position, we are also acutely aware of the potential risks that could impact market stability and will remain vigilant in monitoring developments. Our focus will continue to be on identifying opportunities to improve long-term returns in line with the risk targets for the portfolios. By staying disciplined and opportunistic, we aim to navigate the complexities of the market and position our investments for long-term success.