Since early March we’ve seen a decline in the U.S. stock market that has many investors unnerved. While no one can reliably predict how things will play out in the shorter term, it’s important to understand that markets are often volatile during times of uncertainty—and investors can react strongly when they can’t confidently “price” what’s ahead. In these situations, rather than focusing on the daily or weekly fluctuations, we find that it’s helpful to take a broader view. After very strong performance over the past two years, with U.S. stocks up over 20% in both 2023 and 2024, combined with uncertain news on policy changes, the fact that the markets have recently changed direction is not necessarily surprising.

A Changing Landscape from Early 2025

In our year-end investment commentary, we expressed caution going into the new year and warned that elevated stock valuations, combined with the potential for slower economic growth, could leave us more vulnerable to market volatility. Market reactions to uncertain news – such as significant policy changes – can negatively impact market stability, and indeed this is what we’ve seen recently.

After hitting new highs in mid-February, U.S. stocks have retreated since, and the S&P 500 is now down about 6% as of March 13. Softening economic data points and hotter inflation readings renewed investor concerns over stagflation (high inflation combined with slow growth) while uncertainty over tariffs, immigration, federal layoffs, and the Russia-Ukraine war drove investor sentiment lower. Accelerating trade tensions with Canada in recent weeks have also elevated concerns of a widening trade war that could cause broader economic impact.

Economic Signals are Mixed Amidst Elevated Uncertainty

The U.S. economy has indeed shown signs of slowing in recent months with growth likely to decelerate in the near term. But as always, economic signals are mixed – a reminder not to put too much weight in any given economic data point. While job growth has slowed in recent months, the labor market remains generally healthy and the unemployment rate remains low at 4.1%. Wage growth has outpaced inflation for 21 consecutive months – a positive for consumer spending. Inflation remains above the Fed’s 2% target. While expectations for 2025 interest rate cuts from the Fed are tempered (with an 80% chance of a cut in June) the Fed’s view is that overall monetary policy remains sufficiently restrictive, which suggests rates could remain at current levels or move lower. And while prices of goods subject to tariffs are affected, those price increases tend not to persist beyond when/if tariffs are lifted.

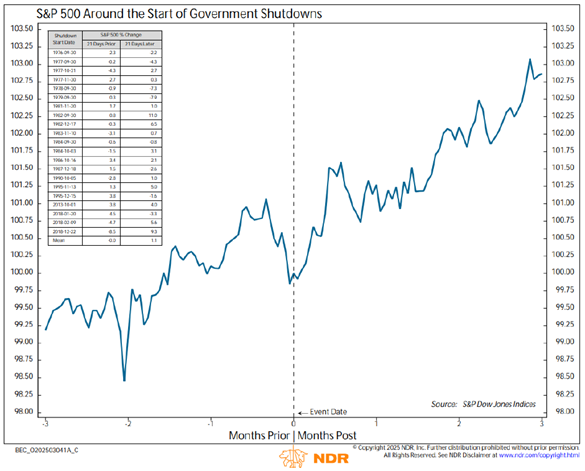

An additional issue is the looming potential for a government shutdown on March 14, with any prolonged closure likely to weigh on GDP growth. However, if Congress follows historical precedent by reaching a last-minute agreement to reopen the government, the economic impact may be temporary. Historically, equity markets tend to decline modestly in the weeks leading up to a shutdown but typically recover in the months that follow (see chart below). This time, however, the shutdown could have a greater impact due to the Department of Government Efficiency’s (DOGE) active efforts to downsize the federal workforce, potentially leading to more disruption than usual.

Govt Shutdown – S&P500 Change; 9/30/1976 – 12/22/2018

All in all, our current research and analysis does not indicate that stagflation or a recession are looming at this point. But clearly, we are also in an overall environment of greater uncertainty and thus more volatility than usual, and this will require careful attention and vigilance in assessing the evolving economic landscape.

Underlying Stock Market Leadership Has Been Shifting

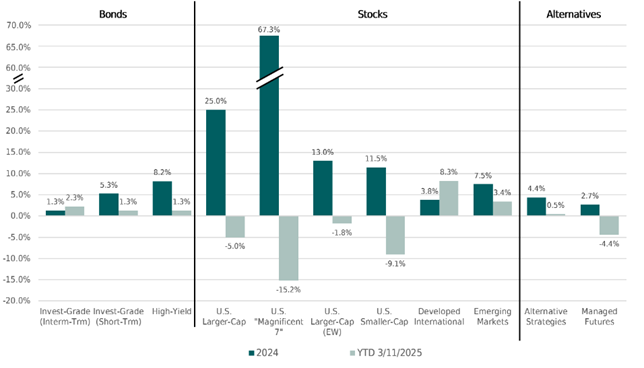

Considering market performance and economic fundamentals, a closer look at industries and sectors tells an additional story, one in which the tech-dominated “Magnificent 7*” companies within the S&P 500 index have given up more ground as earnings have slowed after several years of explosive growth, while the rest of the companies in the market index are seeing better relative performance and stronger earnings forecasts. As seen by the better relative performance of the S&P 500 Equal Weight (EW) index, shown in the chart below, the other 493 stocks (the full index minus the Magnificent 7) have seen accelerating earnings growth after a two-year lull.

Another marker of the shift in market leadership is from growth stocks to value stocks. Over the past few months since the start of the year, the large cap value segment of the U.S. market is down only about 2% while large cap growth is down about 10% (as of March 13). Even looking back as far as five years shows large value edging out large growth (both have double-digit annualized gains over that span).

Meanwhile the U.S. dollar has declined against other currencies, which has helped non-U.S. stocks perform relatively better in recent months – with developed international and emerging market stocks in positive territory year-to-date (see chart below).

Index performance shown is for illustrative purposes only and does not reflect fees or expenses that would reduce actual investment results. Performance reflects index returns as follows (left to right): Bloomberg US Aggregate, Bloomberg US TIPS, Bloomberg US Corporate 1- 3Y, ICE BofA US High Yield, S&P 500, Bloomberg Magnificent 7 TR Index, S&P 500 Equal Weight, Russell 2000, MSCI EAFE, MSCI EM, Wilshire Liquid Alternative, SG Trend Index.

Source: Morningstar Direct. As of 3/11/2025.

Our Investment Positioning

At the portfolio level, our fixed-income exposure continues to favor shorter-maturity high-quality positions that are earning yields above the benchmark. In this uncertain environment, we have taken a bird-in-hand approach, prioritizing attractive absolute returns over trying to predict the timing and magnitude of interest rate moves. Our focus is on bonds that can generate reliable, steady returns that align with our broader investment goals, ensuring we are well-positioned regardless of where market rates head next.

Within the equity allocations, we acknowledge that U.S. equity valuations remain elevated, even with the recent declines. But changing leadership within the equity markets is healthy in our view, and a reminder of the value of diversification, which can both dampen volatility and provide a broader opportunity set. The diversification we create in client portfolios can serve to make the impact from market downturns less severe, as they are designed to help buffer stock market downturns by spreading investments across various asset classes.

While market declines can cause discomfort and test investors’ resolve, they can also create opportunities to enhance longer-term returns through selectively increasing allocations in areas that become compellingly undervalued. This has always been a cornerstone to our approach and will remain a research focus looking ahead.

And for our clients who have taxable investments, we will take the opportunity during market downturns to employ a tax-management approach known as tax-loss harvesting. This involves selling investments that are currently below their purchase price, then reinvesting the proceeds into similar assets. By doing so, the investor can potentially use the capital loss to offset capital gains on their tax returns, reducing their tax burden either this year or in future years.

In Closing

Investment success over the long-term requires a measured focus on fundamentals and avoiding reactive decisions that would be driven by fear in the short-term. By maintaining discipline and using market declines to identify potential investment opportunities in undervalued areas, we can manage through volatility while still positioning portfolios for long-term growth.

Please reach out to your advisor with any questions about this and/or your individual situation.