This year has been eventful for the financial markets, and July saw investors continuing to balance encouraging economic data with uncertainty. Through the end of July, the S&P 500 stock market index reached an all-time high for the year, buoyed by strong earnings reports — especially from large tech firms — as well as growing confidence that the U.S. might avoid a recession, thanks to signs of a resilient consumer and a healthy labor market. Inflation also came in below expectations, though it remains above the Federal Reserve’s long-term target. These positive signs, however, raised questions about how long the Fed may need to keep interest rates elevated.

As we look to the remainder of 2025 and into next year, there are a few key themes we are watching closely, namely trade, the labor market, inflation and monetary policy.

Market Performance

Trade policy remains front and center, though investors seem increasingly less sensitive to these headlines. In late July, the U.S. reached new agreements with both Japan and the European Union. Meanwhile, a key deadline in U.S.–China trade relations was extended as both countries agreed to prolong their current tariff pause by another 90 days. These developments were seen as constructive steps toward greater stability in global trade.

The S&P 500 rose 2.2% during the month of July, driven by continued earnings strength in the technology and communication services sectors. Year to date, this market index is up 8.59% (through July 31). The Nasdaq posted a stronger 3.7% return in the month, supported by continued optimism around AI-driven productivity and corporate investment in infrastructure. Small-cap stocks also moved higher in July, gaining 1.7% (Russell 2000), and are about flat year to date.

Outside the U.S., developed international stocks (MSCI EAFE Index) took a breather, dropping 1.4% in July, yet remain up 17.7% year to date. Emerging market stocks (MSCI Emerging Markets) rose 1.9% in the month of July and are up 17.5% this year to date. Both developed international and emerging markets equities’ performance has been supported by the decline in value of the U.S. dollar during 2025, making them a “hedge” of sorts for the dollar within U.S. dollar denominated portfolios.

Within fixed income, our expectation has been and continues to be that rates will remain volatile and range bound, which was the case in July. The 10-year Treasury yield started the month of July at 4.24% and ended slightly higher at 4.37%. Investment-grade core bonds ended the month down 0.3 % (Bloomberg US Aggregate Bond) but are up 3.7% year to date. Lower quality high-yield bonds were up slightly for the month at 0.4% (ICE BofA US High Yield) and are up 5% year to date as of July 31.

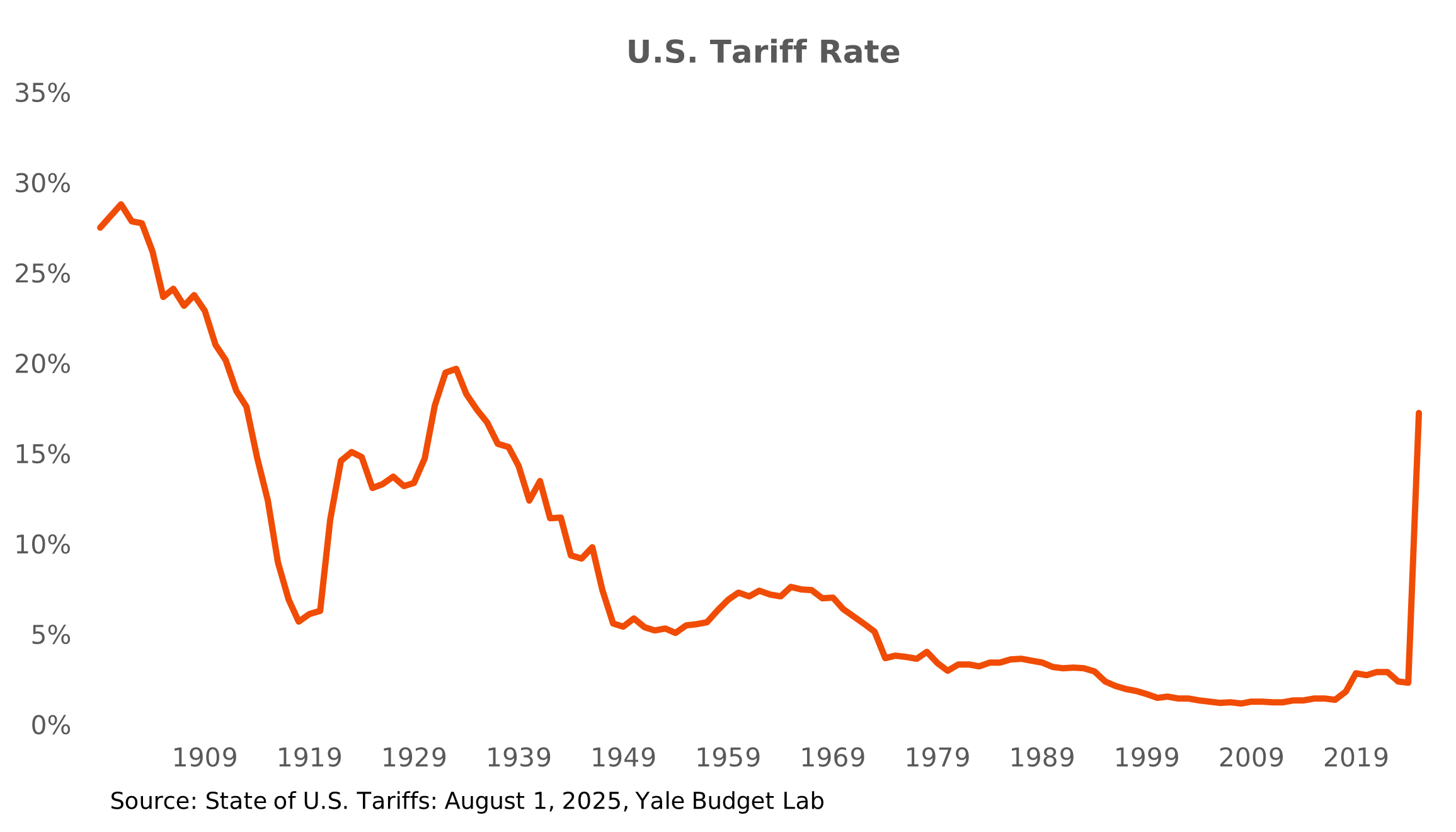

Trade Policy & Tariffs

Tariffs are an important input in our assessment of the economy and markets because they influence how businesses plan, price, and invest. In late July, the U.S. reached trade agreements with major trading partners including Japan and the European Union. These deals brought some welcome clarity. Both trade agreements set a 15% base tariff on most imports from those regions, which is a notable increase from the previous 10% level, but lower than earlier threats of 25% or more. In exchange, Japan agreed to reduce tariffs on U.S. autos and industrial goods and pledged $550 billion in U.S. investments. The EU committed $600 billion through 2028, focusing on sectors like energy and defense.

While the worst-case scenario has been avoided so far, tariffs are still historically elevated and evolving. Some sectors such as steel, aluminum, and copper, remain under pressure, with tariffs as high as 50%. More targeted tariffs are expected soon in industries such as semiconductors and pharmaceuticals. Before we can get a more complete picture, we are also waiting to see what the final agreements are between the U.S. and China and Mexico, both of which have been extended by 90 days.

For perspective on what’s transpired so far this year, tariff levels have jumped from around 2% at the start of the year to between 15% and 20% today. That’s a sharp and broad-based increase, which ends up being a tax on businesses and consumers that is expected to put pressure on the economy.

A key question now is who bears the cost. There’s some indication that foreign suppliers (such as Japanese automakers) are absorbing some of the tariff hit, but it’s still unclear how much of the cost burden will ultimately be passed along to U.S. businesses and consumers. So far, the pass-through of costs to consumers has been more muted than expected, at least for now.

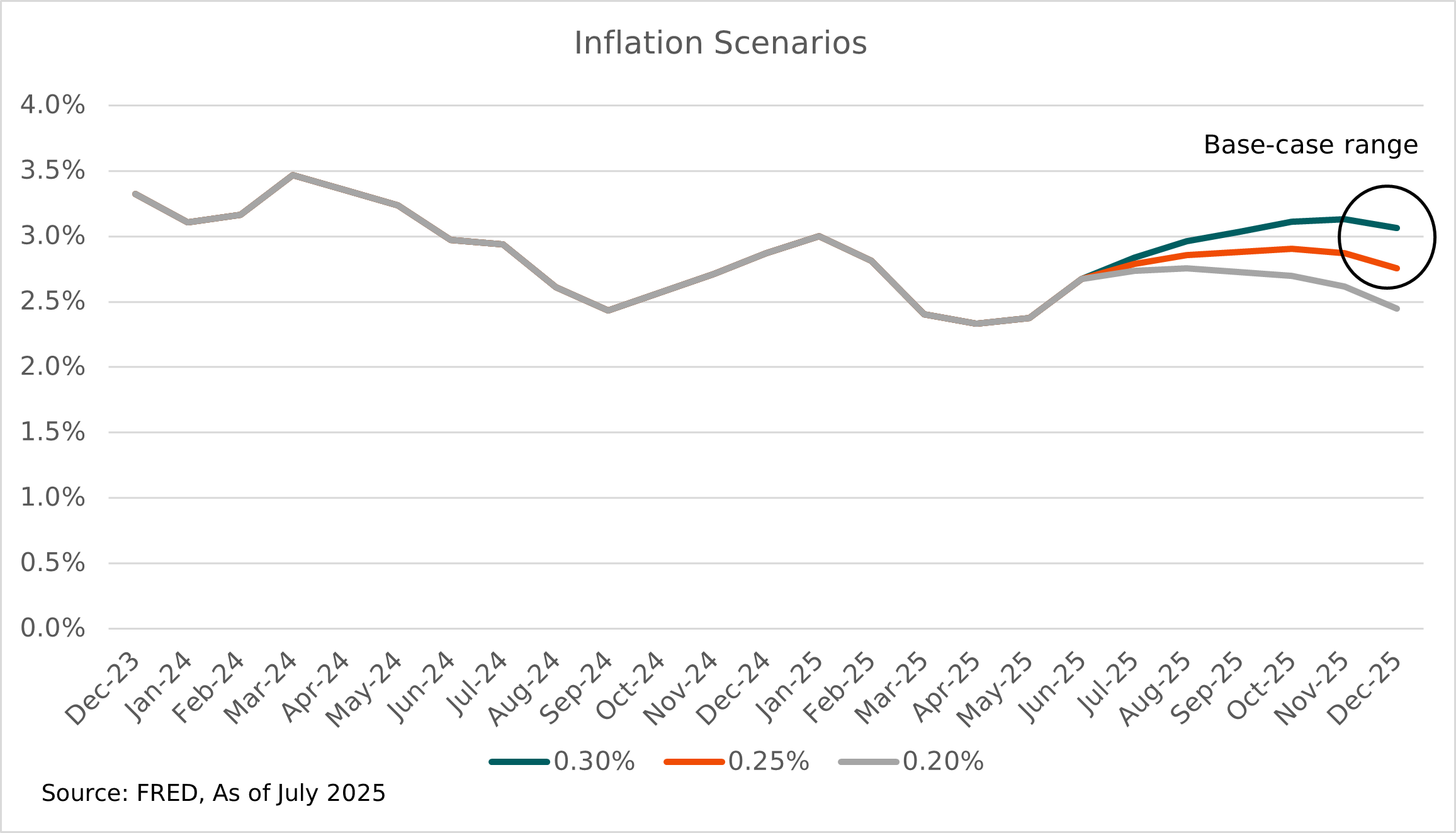

Inflation Outlook

Looking ahead, we expect tariffs will lift inflation over the next few quarters. Our base case economic scenario assumes that core inflation (CPI) will edge up from the current 2.67%, possibly reaching low 3% levels by year-end. This view reflects the delayed impact of these tariffs, which we expect will continue to filter through the economy over the coming months.

The chart below illustrates inflation outcomes using constant month-over-month scenarios through the end of the year.

Chart Disclosure: Illustrative scenario only; assumptions shown; actual outcomes may differ materially.

While recent trade negotiations have brought a bit more stability to expectations, tariffs remain an economic headwind, and we expect they may likely remain a source of cost pressure and policy uncertainty for both businesses and households into 2026. Again, the extent is still unknown, as we think that once businesses have more clarity they can adjust input costs and/or restructure products to help preserve margins and minimize the potential negative impact of price increases.

So far tariffs do not appear to have had a materially negative impact on the economy. Looking ahead, our base case is that the economy may continue to grow but slow down, with GDP possibly falling below 1%, which is still positive. We do not currently see a recession on the immediate horizon.

Labor Market News

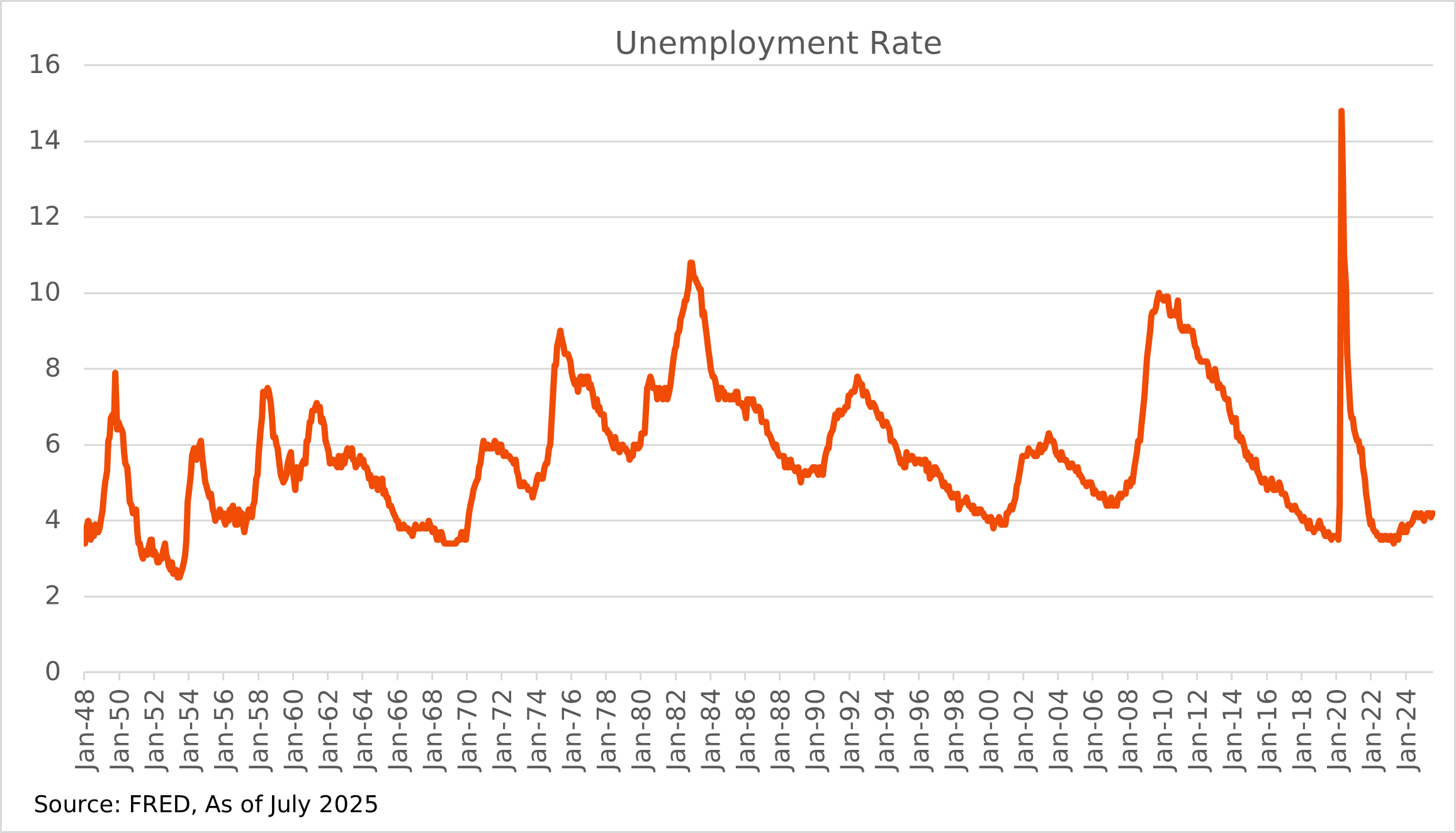

The labor market through July has been a key source of strength. Hiring is soft, but layoffs are still low and that’s been helping to maintain a low and steady unemployment rate. The unemployment rate has been in the low 4% range over the last 12 months. In our modelling we project unemployment to rise gradually but not spike. We have also seen wage growth outpace inflation for 26 consecutive months, which is positive for the economy.

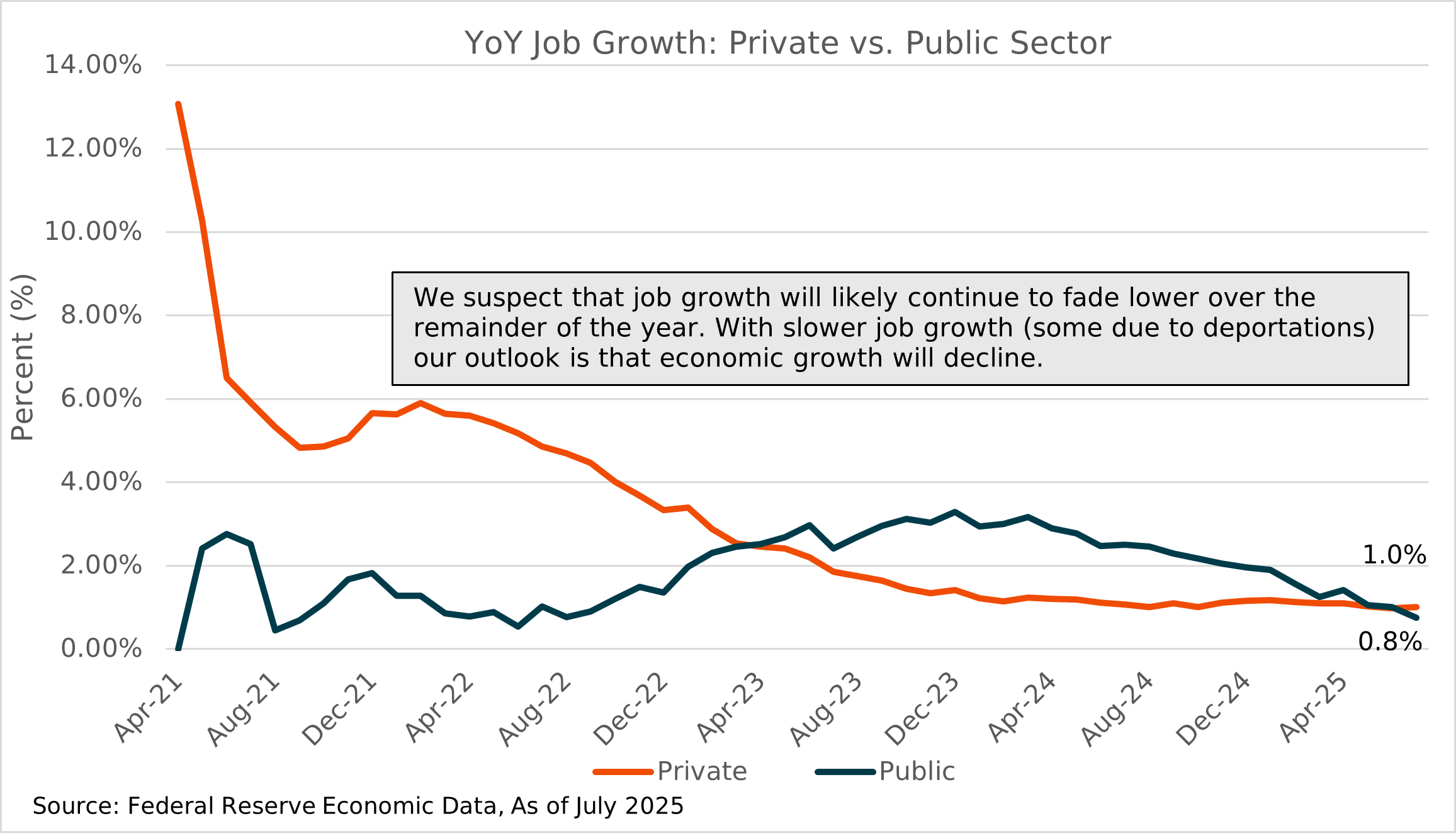

However, it’s not all rosy news from the labor market. One concern is that private sector job growth has been slowing. As shown in the chart below, year-over-year private sector job growth (green line) has declined sharply over the past few years and in recent months it has hovered around the 1% level. With respect to public jobs (blue line), there is also a slowdown of job growth. Overall, these levels of job growth suggest only a modest level of economic growth.

Consumer Spending Continues to Drive the Economy

Meanwhile, the consumer has been holding up in consumption, as evidenced by the latest consumer spending report. Watching consumer data closely is important in assessing economic health, as consumption accounts for roughly two-thirds of the U.S. economy. There are some areas that are weakening, such as non-essentials, but the consumer has support in their higher net worth, with the biggest gains coming from financial assets such as brokerage accounts and 401(k)s (which are at all-time highs), and increasing real asset values, such as homes.

Against the backdrop of full employment and still-elevated inflation, the Fed, as expected, held rates steady in the late-July meeting at 4.25-4.50% for the fifth consecutive meeting. However, it was notable that two Fed governors (Michelle Bowman and Christopher Waller) disagreed, each favoring a 25-basis point rate cut while the rest voted to hold rates steady. It was the first time since December 1993 that two Fed ‑governors formally dissented from a rate decision.

The Federal Reserve’s decision to hold rates steady despite political pressure from President Trump served to underscore its independence, a key pillar of economic stability. This is essential as central bank independence helps anchor inflation expectations, supports market confidence, and helps keep long-term borrowing costs in check. Political interference or abrupt leadership changes risk undermining that credibility, which could increase uncertainty across the economy, and potentially unanchor long-term interest rates.

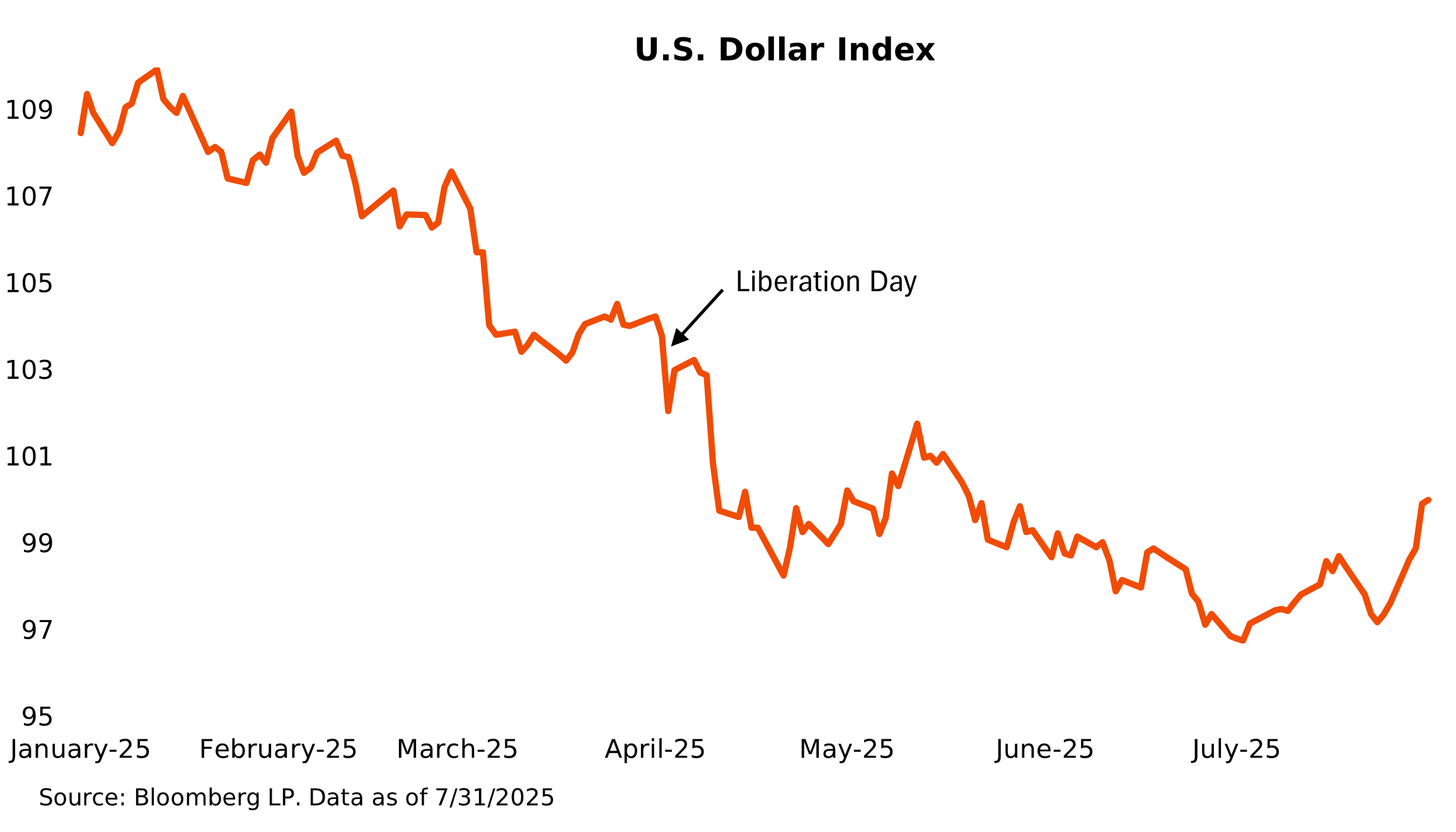

The U.S. Dollar’s Changing Value

Regarding the U.S. dollar, after falling over 10% against other currencies within the first half of the year, it rebounded in July, rising 3.2% even as tariff headlines intensified. Below is a year-to-date chart of the trade-weighted U.S. dollar versus other developed market currencies.

In our view, the dollar generally tracks macro fundamentals but there are periods of disconnect. One key driver is the comparative level of interest rates between the U.S. and other major economies. Higher U.S. rates typically attract capital and support the dollar. The dollar also tends to benefit when markets grow uneasy as it remains the world’s safe-haven currency. Other forces like U.S. fiscal discipline, investor confidence, and relative economic growth also play important roles. Historically, when the U.S. economy outperforms, the dollar strengthens. And while fears about the dollar losing its reserve status are likely overstated, they can still spark volatility.

One indicator we watch closely is the relationship between the trade-weighted dollar and five-year TIPS’ (treasury inflation protected securities) yields, which reflect inflation-adjusted expectations for Fed policy. These usually move together, but through the first half of the year, the dollar has lagged behind rising real yields, which we think signaled investor caution about the U.S. outlook amid renewed trade tensions.

The current level of inflation supports the dollar’s recent move as the Fed was not in a hurry to cut rates. This helped the dollar in July. If the labor market can remain healthy, we believe there could be more dollar strength ahead if inflation momentum persists. But any hint that the economy is weakening, prompting a Fed rate cut, we would likely see the dollar decline.

Investment Implications

Amid the backdrop of macro uncertainty and policy transitions, U.S. equity markets continue to reach all-time highs. Tariff-exposed sectors have remained under pressure, while much of the recent market gains have been concentrated in areas like artificial intelligence (AI)-driven technology, which has seen outsized gains since April. Stock valuations, in our view, offer little cushion for disappointment, with the margin of safety compressing. In this environment, we think a long-term lens is paramount and believe the macro backdrop does not warrant either an overweight or underweight stance by region. For that reason, we are positioning the equity portion of our portfolios to their neutral allocations and further aligning the overall equity allocation with that of the broad global equity markets.

In fixed-income, credit spreads are tight, and yields are now relatively attractive especially in non-traditional parts of the bond market. Our focus remains generally on high-quality fixed income instruments that can deliver attractive levels of income without assuming excess risk from credit or duration levels. We are emphasizing capital preservation and liquidity while monitoring for dislocations in the bond markets that may present longer-term opportunities. As policy and economic signals evolve, maintaining a disciplined, through-the-cycle investment approach will be critical.

Please feel free to contact us or reach out to your Advisor with any questions and/or to discuss your own portfolio and situation.