Second Quarter 2024 Market Recap

In the second quarter of 2024, the U.S. economy stayed resilient in an environment where inflation and interest rates remained higher than expectations. Tighter monetary policy was offset by accommodative fiscal policy, and a still-strong U.S. consumer.

The S&P 500 Index was up nearly 4.5% in the quarter, reaching a new all-time high. The gains came with some volatility in the three-month period. The S&P fell 4.1% in April, pressured by a stronger-than-expected March inflation report and rising bond yields. In May and June, stocks rebounded led by technology stocks. Chip-maker Nvidia became the world’s most valuable company in late-June after its share price climbed to an all-time high, making it worth $3.34 trillion, with its price nearly doubling since the start of this year. We also saw the continuing trend of large-cap stocks (Russell 1000 Index) outperforming small-cap stocks (Russell 2000 Index) and growth (Russell 1000 Growth) beating value (Russell 1000 Value).

Overseas, results were mixed with developed international stocks (MSCI EAFE) falling 0.2%, while emerging markets stocks (MSCI EM Index) rose nearly 5.0%.

Within the bond markets, returns were positive across most fixed-income segments. The benchmark 10-year Treasury yield ended the quarter close to where it started, but rates were volatile in the period. The 10-Year Treasury started at 4.20%, rose to 4.70% before coming back to the mid-4.20% range. In this environment, the Bloomberg U.S. Aggregate Bond Index gained 0.3% and high-yield bonds (ICE BofA Merrill Lynch High Yield Index) were up 1.0% during the quarter.

Overall, economic and corporate fundamentals remained relatively healthy in the quarter, and the next move for the Fed Funds rate is likely to be lower, even if the cuts are taking longer than expected.

Macroeconomic and Investment Outlook

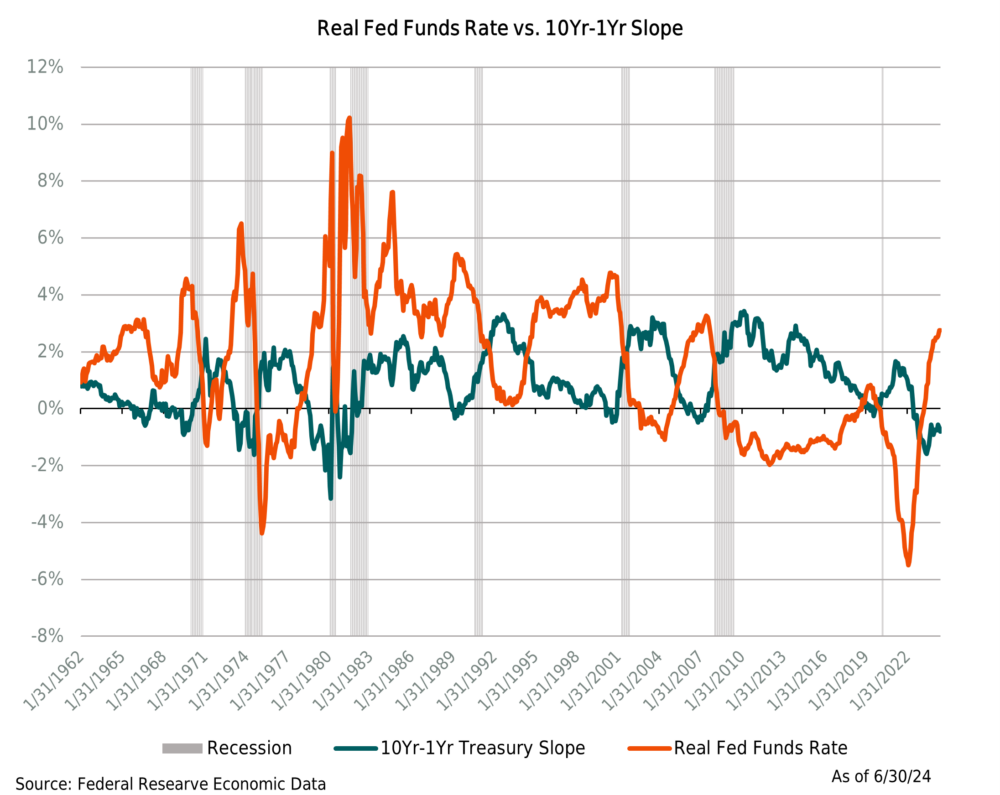

During the second quarter, the U.S. economy began its fifth year of expansion after the brief pandemic-related recession in April 2020. Ongoing economic growth has defied widespread expectations of a recession that were present for most of 2023. Recession concerns were due to the Fed’s rapid and meaningful increase in interest rates resulting in an inverted yield curve (historically a good predictor of recession), and the potential negative impact this would have on the economy. As we laid out in our fourth-quarter 2023 commentary, our view was that given the current level of inflation, Fed policy seemed to be on the border between being accommodative and restrictive.

Our view on Fed policy is largely based on the level of the real Fed Funds rate (Fed Funds rate minus inflation, shown in blue), and prior recessions. (We use the Personal Consumption Expenditures Index, or PCE, the Fed’s preferred inflation metric.) In the chart above, the green line shows the shape of the Treasury curve, with points above zero indicating a normally (upward) sloped yield curve and below zero representing an inverted (downward sloped) yield curve. The vertical grey bars indicate a recession.

We can see that while the yield curve has been inverted since July 2022, Fed policy was very accommodative for most of that time, i.e., the real Fed Funds rates were sharply negative when the curve first inverted. It’s only been more recently that Fed policy moved toward restrictive levels. In prior cycles, real Fed Funds proved restrictive at the 3.5% (or higher) level. To the extent that inflation continues declining, which we think it will, and the Fed keeps rates unchanged, Fed policy will become proportionately tighter, and could start to choke the economy. This is one reason that could support the Fed’s decision to start cutting rates in the second half of the year.

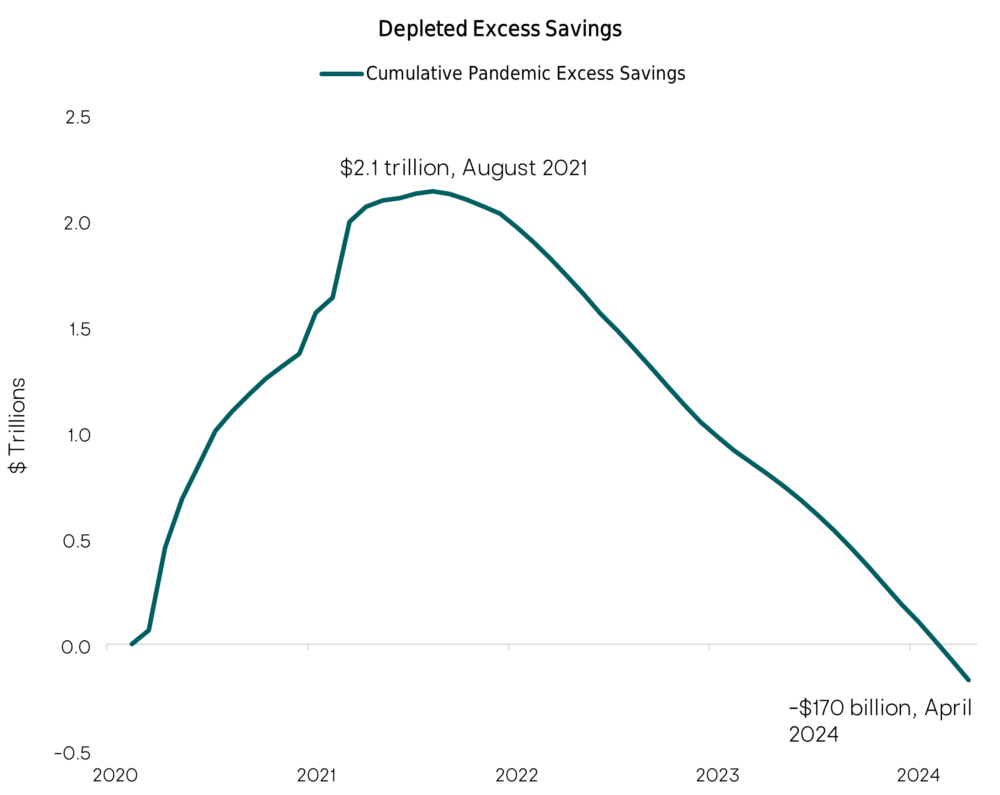

As the economy and corporate earnings have continued to grow, it is apparent that policy has not been too restrictive, or at a minimum, rate increases are taking longer than expected to have an impact. Today, (real) economic growth remains stronger than expected in the 2% to 3% range, a level that is above the Fed’s long-run growth estimate for the U.S. This robust activity seems to have been driven by strong consumer spending despite an erosion of pandemic savings (see chart below).

Source: Bureau of Economic Analysis and San Francisco Fed. Data as of 6/30/2024.

Looking ahead, our base case is for the economy to continue expanding but we suspect the pace of growth will slow over the remainder of the year. We also expect inflation and labor markets will slow but not seize in the near-term, and we think this backdrop could remain supportive for risk assets.

Inflation

Last year, it seemed as though the Fed was decisively winning the inflation battle. But in the first quarter of 2024, particularly in January, inflation came in higher than expected. These elevated readings seem to set the bar higher in terms of evidence the Fed will need to see before cutting rates. As a result, the market dramatically repriced 2024 rate-cut expectations, going from an estimated 6-7 cuts at the start of the year, to 1-2 cuts as of June.

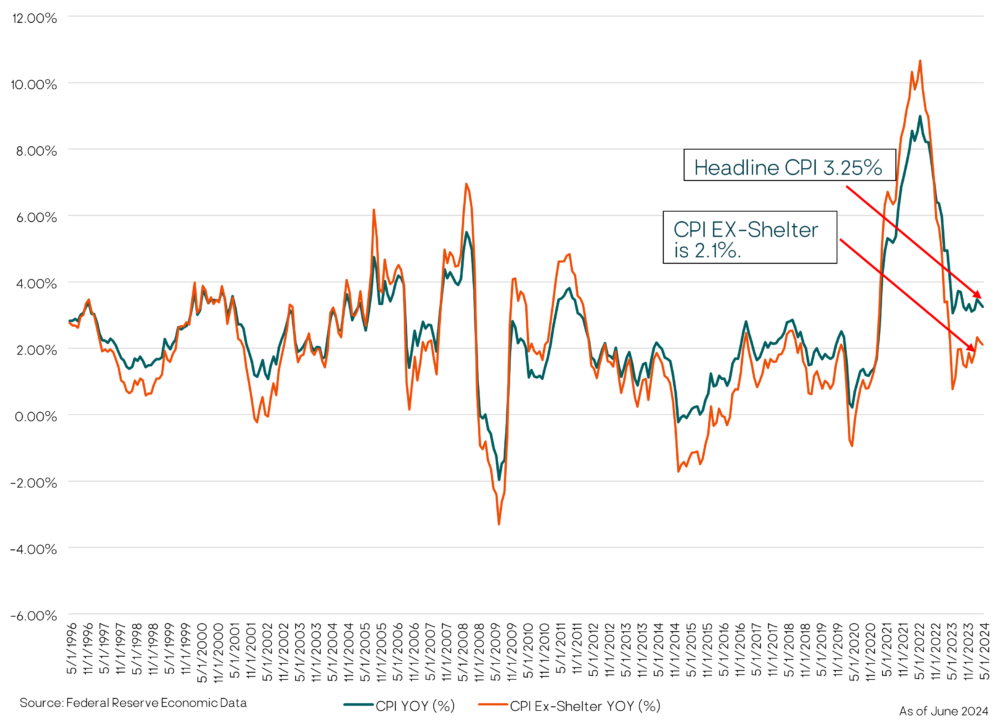

More recently, the April inflation reading showed moderate signs that inflation might again start to trend lower. Our belief has been that despite some higher readings earlier this year, the Fed’s aggressive rate hikes have tamed inflation, and we expect to see continuing disinflation. The Fed targets price rises by the change in the personal consumption expenditures (PCE) deflator, which tracks the prices of a mix of goods and services. By this measure, inflation peaked at over 7% in 2022 and has continued to decline. On the last trading day of June, the latest PCE release came out at 2.6%, down from the 2.7% in May. On a month-over-month basis, PCE was flat. The Core PCE, which excludes food and energy was up 2.6%, and on a monthly basis, Core PCE is up 0.1%, lower than 0.3% in May. During the last Fed meeting, the Fed projected a 2.8% Core PCE for the end of the year, and with that number in mind, they were planning one rate cut in the remainder of 2024. If the data remains at or below their recent year-end estimate, the Fed could cut sooner and more than expected. For now, the market is expecting two rate cuts, with the first in September and the second in December. A second popular inflation indicator, the Consumer Price Index (CPI), has followed a similar pattern as PCE, peaking at 9% in 2022, and falling to its current level of 3.25%.

We should highlight that on a year-over-year basis, U.S. core CPI is running higher than U.S. core PCE, and in fact, most foreign developed market core inflation measures. Only U.K. CPI is higher than U.S. CPI, at over 4%. A primary reason behind the higher U.S.CPI number, whether compared to PCE or other foreign developed markets, is the much higher weight it assigns to owners’ equivalent rent (OER). OER is an estimate of the cost of homeownership, or the rent a homeowner would pay for a similar property nearby. While we have several questions about the OER approach and its accuracy, we believe the CPI number will continue to decline over the course of the year and into next year.

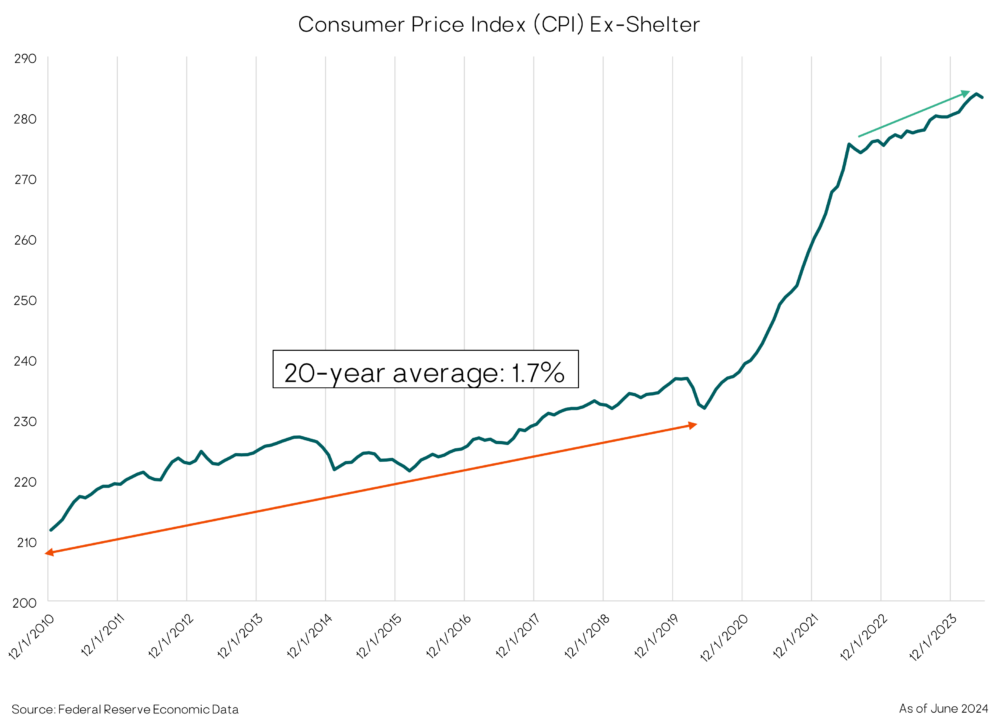

The chart above shows CPI and CPI ex-Shelter. If you exclude shelter from CPI, you can see that inflation has been tamed at or around 2% since May of 2023. We expect the shelter component to gradually decline over the remainder of the year, albeit not in a straight line, and thus CPI too. The chart below shows that since mid-2022, CPI ex-shelter has increased at 1.44% annualized and the average over last 12 months is 1.76%. The most recent reading is 2.1%. In other words, across most of the economy, price increases have been in line with the Fed’s target.

Indeed, the Fed is in somewhat of a tight spot. It has and continues to repeat its commitment of 2% inflation as measured by the PCE deflator. Changing course now could cause the market to question the Fed’s commitment to that target, with the worry being that the Fed loses credibility. In the meantime, many investors are wondering if we’ll ever reach this target; it’s the economy’s version of waiting for Godot. It seems that the Fed is concerned about a second wave of inflation, and without strong evidence of an imminent recession, they will be reluctant to cut rates aggressively. The risk of keeping rates too high for too long is that the Fed sacrifices the economy in the near-term for the sake of reaching what seems to be a sacrosanct target. We suspect the Fed could attempt to justify rate cuts before reaching the 2% target by pointing to near-term trends of 3- and 6-month annualized rates of inflation, which could be below their target.

We believe the Fed is inclined to cut rates this year, recognizing the risks of waiting too long. Our sense is that some Fed officials recognize higher rates are causing some economic strains in areas such as commercial real estate, regional banks, and lower-end consumers, and that some of today’s offsetting factors such as fiscal policy might not last forever. Furthermore, we suspect there is some risk to smaller-cap companies if rates remain elevated for much longer. Smaller-cap companies have a meaningful amount expensive floating-rate debt that is tied to short-term rates, and that is nearing maturity. The Fed certainly doesn’t want to cause a recession when it’s unnecessary, and that’s the fine line they are walking today.

One prevailing question in the market is whether the U.S. presidential election will impact the timing of Fed policy changes. But let’s assume the Fed wants to delay cutting rates because they are concerned about the optics of appearing political ahead of an election; isn’t that in and of itself political?! Fed Chair Powell has stated that the looming U.S. presidential election will not influence the Federal Reserve’s interest-rate decisions, and that Fed policy decisions will be guided by the data and how those data affect the outlook and the balance of risks. Let’s hope that’s the case.

The Consumer

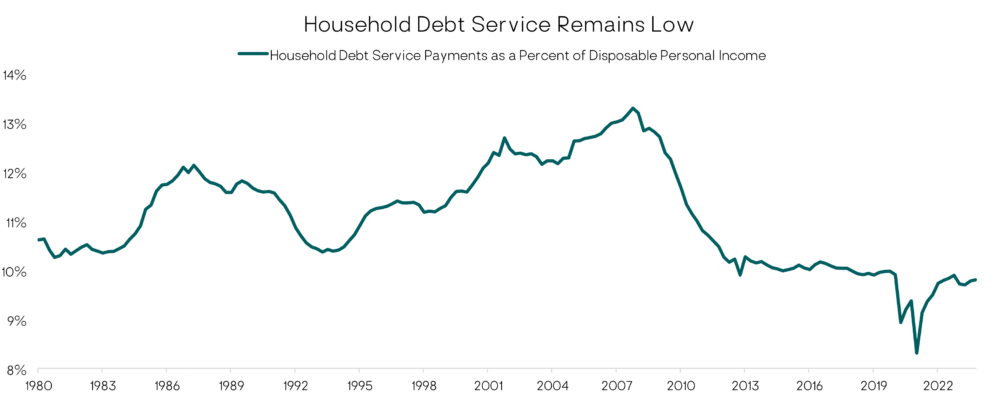

The consumer has driven U.S. economic growth for the past three years, thanks to improvement in both employment and real wages. The strong consumer has surprised many, given the headwinds of higher interest rates and inflation. However, it’s worth pointing out that U.S. consumers are not highly levered like they were prior to the Financial Crisis (see debt service chart below). The consumer debt service ratio (household debt service payments as a percentage of personal income) remains sub 10%. Moreover, while interest rates and mortgage rates have increased significantly, their impact on the economy has been softened by the fact that the share of homes without a mortgage has risen to roughly 40%, and that nearly half of all mortgages outstanding have fixed rates below 4%.

Source: Board of Governors of the Federal Reserve System. As of 12/31/2023.

That said, there are signs the U.S. consumer may be slowing. Recent data have pointed to declining consumer sentiment as a warning sign of slower spending ahead. The University of Michigan Consumer Sentiment Index fell to a seven-month low in June, indicating a pessimistic view of personal finances. In the May retail sales report, growth was positive but slower than expected. This recent data point suggests consumers are exercising more caution amid tighter budgets. Specifically, headline sales rose 0.1% from the prior month versus the consensus for a 0.3% rise. In our view, consumption growth is slowing as high borrowing costs and high prices are starting to bite. Certainly, inflation has slowed since the peak in 2022, but prices have increased more than 20% cumulatively since 2020 based on CPI, and consumers are not excited that prices are rising at a slower pace. This is especially true for lower-income consumers, who feel the impact of inflation when buying essentials such as rent, food, and gas.

So far, any concerns around the consumer have not seemed to scare investors. Investors have pushed the S&P 500 to more than 30 new highs this year as the economy has grown at nearly 3% (in real terms) over the past four quarters. But as excess savings shrink (see earlier chart), the impact of inflation is more painful. We would characterize this process as a normalization after a period of splurging, rather than something more ominous in the near term. Therefore, we are currently viewing this as a yellow light and not a red one. But looking ahead, we will be monitoring the labor market and the consumer for signs of further deterioration, which could impact our positioning.

Equity Markets

At the end of June, our portfolios’ equity exposures remain at their neutral strategic weights across the U.S., developed international, and emerging markets.

After falling 4% in April, global stocks rebounded in May and June with the MSCI ACWI Index gaining nearly 3% for the quarter. U.S. stocks again led the charge with all three major indexes – the Dow Jones, Nasdaq, and S&P 500 all making new all-time highs in the quarter.

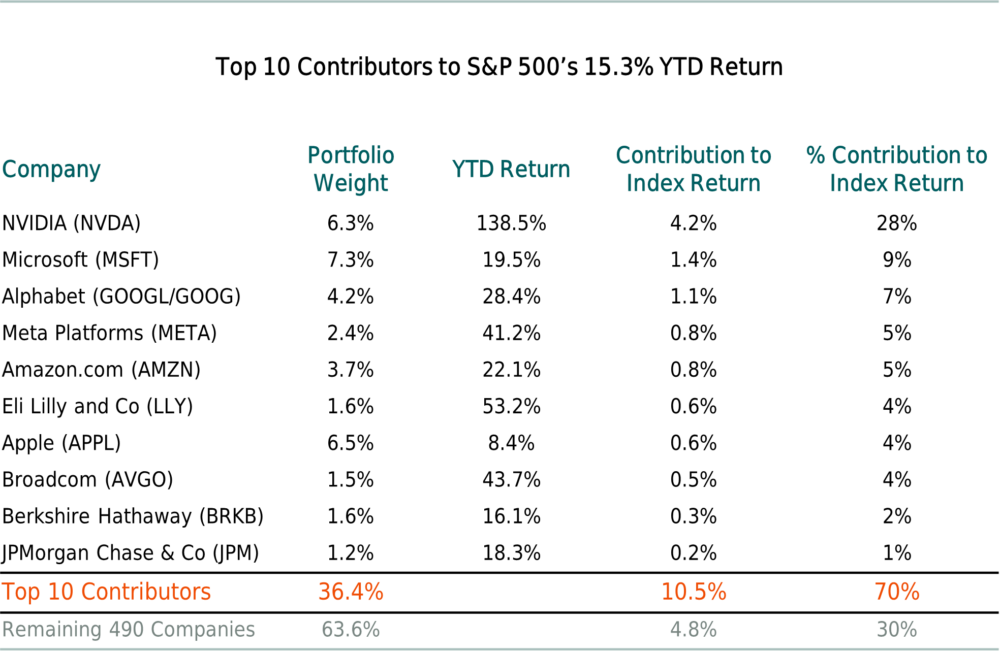

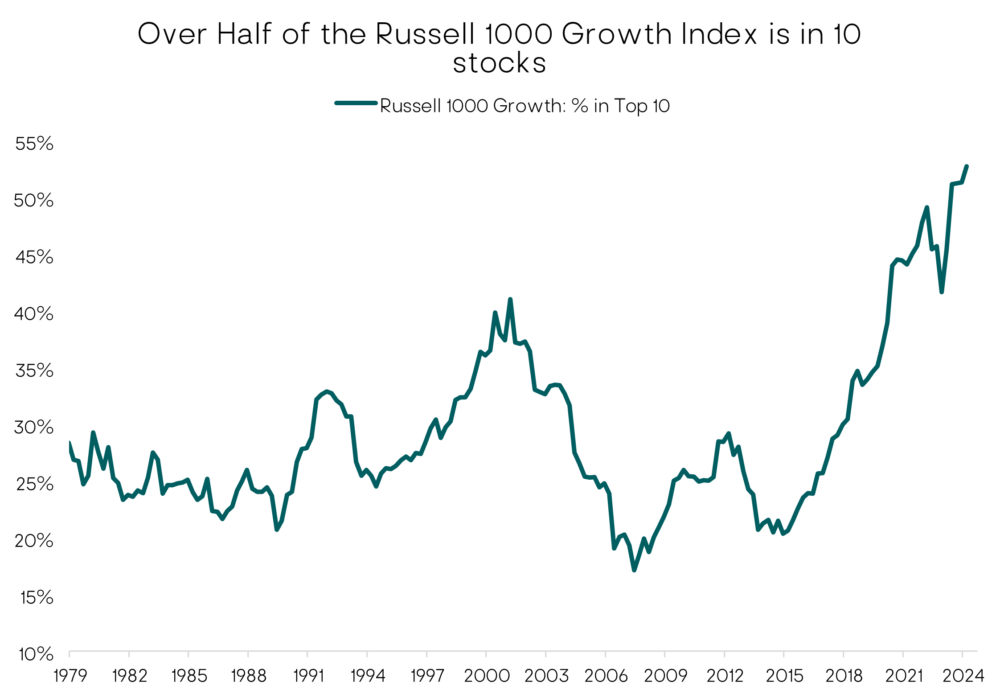

Continuing the theme from 2023, an even smaller handful of U.S. mega-cap technology stocks continue to lead the way higher for the domestic equity market (S&P 500 Index). Last year just 30% of stocks within the S&P 500 outperformed the index. This was a historically low figure—a level not seen since the late-1990s. Yet, so far in 2024, the concentration of returns moved even higher. Through late June 2024, only 27% of stocks are outperforming the S&P 500. This is lowest reading on record going back more than 50 years. As shown in the table below, the top 10 contributors in 2024 have accounted for 70% of the S&P 500’s 15% year-to-date return. We should note that growth indexes have become even more concentrated. The 10 largest stocks in the Russell 1000 Growth Index now account for more than 50% of index. This is the highest level of concentration since its inception in the late 1970s.

Source: Morningstar Direct. S&P 500 Index proxided as iShares Core S&P ETF. Data as of 6/24/24.

While the concentration levels at the index level are noteworthy, it’s possible that this trend can continue for some time. Afterall, the strong run for Artificial Intelligence (AI) stocks has been supported by companies such as Nvidia which continue to deliver and beat earnings estimates.

Our portfolios have meaningful exposure to many of these mega-cap stocks through the exchange-traded funds and mutual funds we utilize. But we remain balanced, also owning larger-cap value and smaller-cap U.S. stocks that are trading at more attractive valuations and offer important diversification benefits. Smaller-cap U.S. stocks, for example, are trading at valuations relative to large-cap stocks that have not been seen in years, dating back to the late 1990’s. We should also note that we think it’s quite possible that areas of the U.S. equity market which have lagged and have lower valuations — small-cap companies and value stocks — could benefit from an ongoing expansion and a broadening out of the market rally.

Source: Morningstar Direct. Data as of 5/31/2024.

Outside of the U.S., there are some compelling opportunities in developed international (MSCI EAFE) and emerging-market stocks (MSCI EM). Europe, for example, is home to several leading businesses in a range of growing and attractive sectors. For instance, Novo Nordisk has seen its stock price double over the past two years following the successes of its type-two diabetes drug Ozempic, and its weight-loss drug, Wegovy, becoming Europe’s largest company. Within the consumer discretionary sector there are world-leading European luxury brand companies such as LVMH, which now also constitutes a significantly larger proportion of the European equity index (MSCI Europe), as it has benefited from growing consumption from the rising middle-class populations in emerging economies.

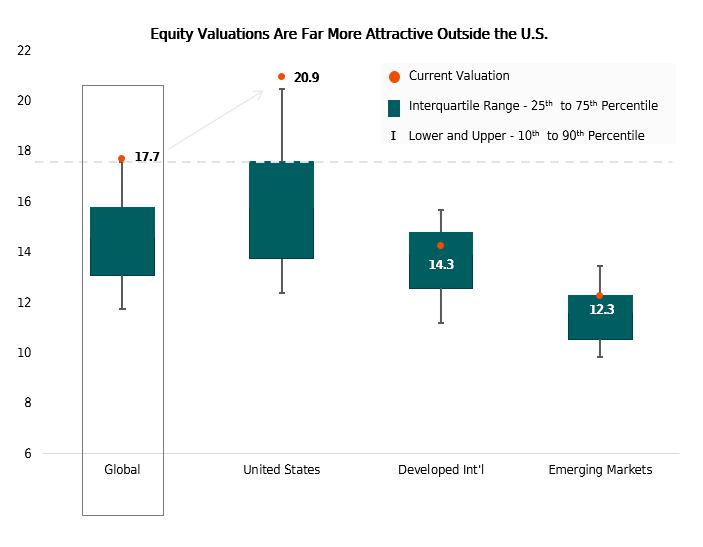

From a valuation perspective, the discount for developed international stocks versus the U.S. is the widest it’s been in decades. From 2006 through 2016, the U.S. and developed markets traded within one multiple point of each other. The average forward P/E for the S&P 500 over the period was 14x compared to 13x for MSCI EAFE. Since 2016, the valuation gap has widened substantially. The S&P 500 now trades at nearly 21x forward earnings, while the MSCI EAFE remains close to 14x. The story can be seen in the chart below. U.S. stocks trade near peak valuations, while other regions offer better relative values as their valuations are not as extended. All else equal, lower starting valuations imply better long-term returns and should provide more of a valuation cushion if P/E multiples contract in a stock market sell-off.

Source: Bloomberg LP. From 1/1/2006 to 6/30/2024.

While relative valuation gaps between different geographic stock markets may be a reason to overweight one versus another — we believe one should also factor in absolute valuation levels for tactical positions. Given that neither developed international nor emerging-market stocks are cheap on an absolute basis, we do not think a tactical position in these regions is warranted.

On the global stage, there are a significant number of elections in 2024 and a rise of political uncertainty has and will likely bring volatility to the markets. For example, in mid-June, we saw volatility jump in France, a response to the decision by French President Macron to call a snap election after his party had disappointing results in the European Parliamentary elections. The markets were taken by surprise by the announcement of an early election and the reaction focused on the Eurozone markets and more particularly French securities. French government bonds tumbled, driving yields spreads over safer German bonds to the highest level in seven years. European stocks also declined though the drop was more pronounced in France, with Eurozone bank stocks getting hit the hardest, particularly French banks.

Of course, here in the U.S., we expect pockets of volatility as the drumbeat of the November election gets lounder, particularly given today’s polarized political environment. Undoubtedly, headlines will influence short-term market fluctuations but longer-term, fundamentals are what drive market performance. Our focus will continue to be on factors such as Fed policy, economic growth, inflation, fiscal imbalances, valuations, etc. Our intention is not to minimize the importance of the election, but to point out that the gears of the economy are not overhauled based on an election outcome. For example, the U.S. economy is consumer driven and that’s not going to change. Ultimately, the fundamentals of the economy don’t change overnight, and we don’t think an investment strategy should either. Our approach will be to stay disciplined and be on the lookout for opportunities that arise with market fluctuations.

Fixed-Income/Bond Markets

Bonds came into 2024 on a high note after ending 2023 with strong performance, and it seemed that the days of losses were behind us. After all, the economy was growing, inflation had declined meaningfully and consistently since mid-2022, the Fed was discussing rate cuts, and unemployment remained low. But then inflation and job growth came in higher than expected causing a dramatic reduction in the number of expected rate cuts. This created an unusual level of interest-rate volatility and questions mounted around Fed policy, pushing yields higher. This resulted in more attractive income for most fixed-income sectors, and this higher income will serve as a buffer against a move higher in rates.

As mentioned above, the Fed’s latest forecast is for one cut over the remainder of 2024, and then four cuts over the next two calendar years. The current market consensus is for one to two cuts this year. Our view is that longer-term interest rates (the 10-year Treasury) will be rangebound between 4.0% and 4.75% in 2024, and we would not be surprised to continue seeing sharp movements in yields within this range as the market continues to react to economic data and try to anticipate the Fed’s next move. As we look to next year, we would not be too surprised to see longer-term rates in the 3.5% to 4.0% range as the Fed reduces rates. Regarding short-term rates, we think the Fed will cut up to two times this year and potentially four times in 2025. Should we face a recession, today’s current level of rates (5.25% to 5.50%) gives the Fed plenty of room to cut rates aggressively to prevent a protracted slowdown, although we don’t expect short term rates to return to 0%.

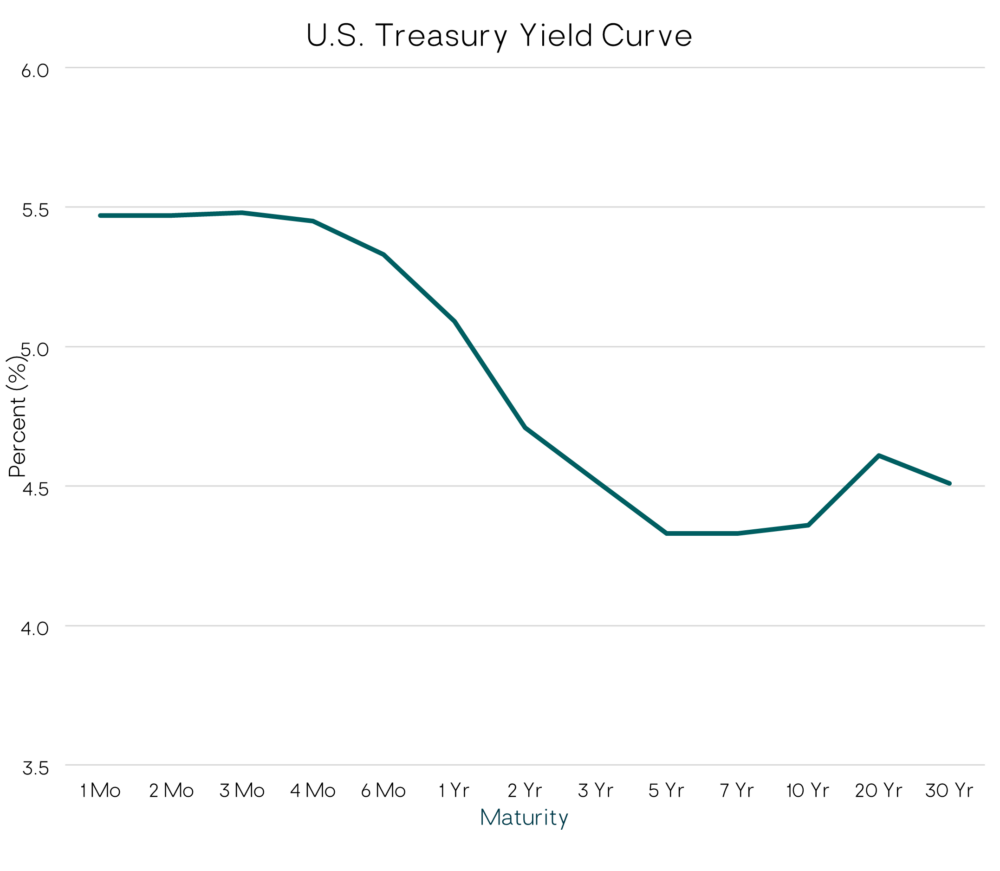

In the meantime, the yield curve (shown below) remains inverted, meaning short-term bonds yield more than longer-term bonds. Ultimately, we will have to return to a normal-shaped yield curve, where investors receive higher yields for longer maturities. As we show in the chart below, investors are receiving slightly more than 1% additional yield for investing in short-term bonds compared to the 10-year Treasury, with less interest-rate sensitivity.

U.S. Department of The Treasury. Data as of 6/30/2024.

At the end of June, 3-month Treasury bonds were yielding 5.48% compared to 4.36% for the 10-year Treasury. If we consider potential changes to the yield curve over the next two years, one possible outcome is that the Fed funds rate is 225 basis points (bps) lower, an estimate based on the Fed’s projection of nine rates cuts by the end of 2026. This would put the 3-month Treasury yields in the 3.0% to 3.25% range. If we assume a normal term-yield premium, it’s likely the 10-year Treasury would be in the mid to upper 3% range. From current yield levels of 4.36%, this limits the upside price potential as longer-term bond yields only have so much room to decline.

This outlook, combined with our view that inflation is under control for now, and that short-term interest rates have peaked and will likely move lower explains our fixed-income portfolio positioning. We maintain meaningful exposure to short-term bonds, taking advantage of the inverted yield curve, emphasizing shorter-term higher-yielding securities with yields in the 6.5% to 7% range, while also maintaining some exposure to longer-term bonds with yields in the 4.5% to 5%, which can also provide protection in the event of a stock-market downturn.

Our rationale for our short-term exposure is as follows. If rates are unchanged, we benefit from holding short-term bonds with their elevated yields, while still earning an attractive yield on the longer-term core bonds. If long-term yields move higher (prices move lower as yields increase), short-term bonds will hold their value and outperform long-term bonds and with less volatility. Where short-term bonds could lag meaningfully is if longer-term yields move materially lower (prices higher). This would occur during a flight to safety, likely due to recessionary concerns. For example, in the scenario where short-term rates are unchanged and long-term rates fall 100 bps, short-term bonds will lag but would still produce an attractive return (6.5% to 7%) compared to a low double-digit return for longer-term bonds. There could also be a scenario where the Fed is cutting short-term rates, which would further benefit short-term bond returns, and we could see returns in the 7.5% to 8.0% range. The bottom line is that portfolios benefit from owning short-term bonds in the flat- to higher-rate scenarios, while still participating in the lower-rate scenarios. We think winning in two out of three scenarios, but still generating an attractive return if we “lose” in the third scenario, warrants an allocation.

Regarding corporate bonds, defaults remain below average. According to JP Morgan, high-yield bond and loan default rates are 1.8% and 3.1%, respectively, which are 1.09% and 0.17% below levels at the start of the year. While we expect to see defaults move moderately higher over the remainder of the year, we do not foresee a near-term risk of a spike in default rates given still-attractive corporate fundamentals. We do have some exposure to below-investment-grade securities, where we are finding attractive opportunities. While the yield spreads in this space are below average and appear expensive, the portfolio exposure we have is higher-quality with shorter-term maturities than the high-yield market and we do not think we are stretching on the risk continuum to achieve these yields. We are only giving up incremental yield by seeking more conservative exposure in this space, and we think we are being appropriately compensated for this exposure.

Looking ahead, we will be on the lookout for opportunities. A specific opportunity we are monitoring is longer-term interest rates. If we see a meaningful increase in these yields, it is likely that we would increase exposure to high-quality, interest-rate sensitive securities to capture attractive yields and provide more ballast to the portfolios. Conversely, if we benefit from a meaningful decline in longer-term bond yields, it’s possible we could further increase our exposure to short-term bonds.

Alternatives Strategies

The first six months of 2024 showed that creating a diversified portfolio using only traditional assets can be difficult. Earlier this year when concerns about reaccelerating inflation surfaced, stocks and bonds were positively correlated on the downside, i.e., bonds did not serve as a portfolio ballast. For example, in this environment, trend-following managed futures (SG Trend Index) provided strong returns and meaningfully outperformed the Bloomberg Aggregate Bond Index (the “bond market”). The year-to-date performance demonstrates that managed futures strategies can produce attractive returns in different market environments and are not just a hedge against bond and stock declines. We continue to believe managed futures are a good diversifier given their potential to deliver uncorrelated returns outside of traditional asset classes/asset allocation.

In Closing

The U.S. economy looks set to benefit from a continuing gradual moderation in growth, inflation, and jobs, creating a backdrop that could support risk assets. As was the case last quarter, the stock market continues to hit new highs as economic growth continues to benefit corporate earnings. U.S concentration remains high with the Magnificent Seven representing over 25% of the S&P 500. There’s no doubt that the other 493 stocks of the S&P 500 have struggled on a relative basis, but they could be set to move higher if the key economic drivers outlined above continue to fuel the economy. That said, fears of a recession haven’t completely abated. Looking out to the end of the year and into next year, the question remains whether a recession will be avoided or delayed. As such, we are keeping a close eye on the typical drivers of recession, including the labor market, consumer spending, and corporate earnings, where a deterioration in these variables could influence portfolio positioning.

Heading into the second half of the year, we continue to anticipate pockets of volatility given headline risks related to Fed policy, geopolitical events, and the upcoming U.S. presidential election. In the event of volatility, we will look to be opportunistic, taking advantage of any attractive risk/reward opportunities that arise.

We thank you for your continued confidence and trust.

– Litman Gregory Wealth Management

Important Disclosure

This report is solely for informational purposes and shall not constitute an offer to sell or the solicitation to buy securities. The opinions expressed herein represent the current views of the author(s) at the time of publication and are provided for limited purposes, are not definitive investment advice, and should not be relied on as such.

The information presented in this report has been developed internally and/or obtained from sources believed to be reliable; however, Litman Gregory Wealth Management, LLC (“Litman Gregory” or “LGWM”) does not guarantee the accuracy, adequacy or completeness of such information. Predictions, opinions, and other information contained in this article are subject to change continually and without notice of any kind and may no longer be true after the date indicated.

Any forward-looking statements speak only as of the date they are made, and LGWM assumes no duty to and does not undertake to update forward-looking statements. Forward-looking statements are subject to numerous assumptions, risks and uncertainties, which change over time. Actual results could differ materially from those anticipated in forward-looking statements.

In particular, target returns are based on LGWM’s historical data regarding asset class and strategy. There is no guarantee that targeted returns will be realized or achieved or that an investment strategy will be successful. Target returns and/or projected returns are hypothetical in nature and are shown for illustrative, informational purposes only. This material is not intended to forecast or predict future events, but rather to indicate the investment returns Litman Gregory has observed in the market generally. It does not reflect the actual or expected returns of any specific investment strategy and does not guarantee future results. Litman Gregory considers a number of factors, including, for example, observed and historical market returns relevant to the applicable investments, projected cash flows, projected future valuations of target assets and businesses, relevant other market dynamics (including interest rate and currency markets), anticipated contingencies, and regulatory issues. Certain of the assumptions have been made for modeling purposes and are unlikely to be realized. No representation or warranty is made as to the reasonableness of the assumptions made or that all assumptions used in calculating the target returns and/or projected returns have been stated or fully considered. Changes in the assumptions may have a material impact on the target returns and/or projected returns presented.

A list of all recommendations made by LGWM within the immediately preceding one year is available upon request at no charge. For additional information about LGWM, please consult the Firm’s Form ADV disclosure documents, the most recent versions of which are available on the SEC’s Investment Adviser Public Disclosure website (adviserinfo.sec.gov) and may otherwise be made available upon written request to compliance@lgam.com

LGWM is an SEC registered investment adviser with its principal place of business in the state of California. LGWM and its representatives are in compliance with the current registration and notice filing requirements imposed upon registered investment advisers by those states in which LGWM maintains clients. LGWM may only transact business in those states in which it is noticed filed or qualifies for an exemption or exclusion from notice filing requirements. Any subsequent, direct communication by LGWM with a prospective client shall be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides.

Index Disclosure

Any reference to a market index is included for illustrative purposes only, as it is not possible to directly invest in an index. Indices are unmanaged, hypothetical vehicles that serve as market indicators and do not account for the deduction of management fees or transaction costs generally associated with investable products, which otherwise have the effect of reducing the performance of an actual investment portfolio.

The Dow Jones Industrial Average measures the stock performance of 30 leading blue-chip U.S. companies.

The Standard & Poor’s 500 Composite Stock Price Index is a capitalization-weighted index of 500 stocks intended to be a representative sample of leading companies in leading industries within the U.S. economy. Stocks in the Index are chosen for market size, liquidity, and industry group representation.

The Russell 1000 Index ® measures the performance of the 1,000 largest companies in the Russell 3000.

The Russell 1000 Growth Index ® measures the performance of those Russell 1000 companies with higher price-to-book ratios and higher forecasted growth values.

The Russell 2000 Index measures the performance of the small-cap segment of the US equity universe. The Russell 2000 Index is a subset of the Russell 3000® Index representing approximately 7% of the total market capitalization of that index, as of the most recent reconstitution. It includes approximately 2,000 of the smallest securities based on a combination of their market cap and current index membership.

The MSCI ACWI Index represents the performance of large- and mid-cap stocks across 23 developed and 24 emerging markets. The index covers 2,900 constituents across 11 sectors and approximately 85% of the free float-adjusted market capitalization in each market.

The MSCI EAFE Index is an equity index which captures large and mid-cap representation across 21 Developed Markets countries* around the world, excluding the US and Canada. With 799 constituents, the index covers approximately 85% of the free float- adjusted market capitalization in each country.

The MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance of emerging markets. The MSCI Emerging Markets Index consists of the following 23 emerging market country indexes: Brazil, Chile, China, Colombia, Czech Republic, Egypt, Greece, Hungary, India, Indonesia, Korea, Malaysia, Mexico, Peru, Philippines, Poland, Qatar, Russia, South Africa, Taiwan, Thailand, Turkey and the United Arab Emirates.

The MSCI Hedged Indexes include all of the securities and weights of each corresponding unhedged MSCI Parent Index, enabling investors to measure the impact of hedging currency, for all the constituents of the Parent Index.

MSCI World ex USA Index: captures large and mid cap representation across 22 of 23 Developed Markets (DM) countries*–excluding the United States. With 871 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country.

The MSCI Europe Index is a free float-adjusted market capitalization index that is designed to measure developed market equity performance in Europe. As of June 2007, the MSCI Europe Index consisted of the following 16 developed market country indices: Austria, Belgium, Denmark, Finland, France, Germany, Greece, Ireland, Italy, the Netherlands, Norway, Portugal, Spain, Sweden, Switzerland and the United Kingdom.

The Bloomberg U.S. Aggregate Bond Index is a broad-based benchmark that measures the investment grade, U.S. dollar- denominated, fixed-rate taxable bond market.

The US High-Yield Market Index is a US Dollar-denominated index which measures the performance of high-yield debt issued by corporations domiciled in the US or Canada.

The ICE BofA US High Yield Index is market capitalization weighted and is designed to measure the performance of U.S. dollar denominated below investment grade (commonly referred to as “junk”) corporate debt publicly issued in the U.S. domestic market.

The ICE U.S. Dollar Index is a geometrically-averaged calculation of six currencies weighted against the U.S. dollar.

The SG Trend Index, also known as the SG Trend-Sub Index, is a market-based performance indicator that tracks the daily rate of return for the 10 largest trend-following CTAs (commodity trading advisors) in the managed futures space. The index is equally weighted and designed to correlate with the returns of trend-following strategies.

The S&P/LSTA Leveraged Loan 100 Index (LL100) dates back to 2002 and is a daily tradable index for the U.S. market that seeks to mirror the market-weighted performance of the largest institutional leveraged loans, as determined by criteria. Its ticker on Bloomberg is SPBDLLB.

Estimated Returns Disclosure

Scenario Definitions:

Downside: The economy falls into a deep and sustained recession for any of various reasons, such as deleveraging/deflation, unexpected systemic shock, geopolitical conflict, Fed or fiscal policy error, etc. At the end of our five-year tactical horizon, S&P 500 earnings are below their normalized trend and valuation multiples are below-average reflecting investor risk aversion. Inflation and 10-year Treasury nominal and real yields are very depressed.

Base: Consistent with long-term economic and market history, reflecting economic and earnings growth cycles that are interspersed with recessions around an upward sloping normalized growth trendline. Inflation is at or moderately higher than the Fed’s 2% target level and 10-year Treasury real yields are around zero percent to slightly positive. For the S&P 500, we now bookend our base case with a lower-end and upper-end estimate:

-

At the lower end of our base-case fair-value range, reflation efforts are successful and nominal economic growth is higher than the average. However, the economy overheats, and valuation multiple and some margin compression largely offset the favorable macro backdrop.

-

At the upper end, reflation efforts are also successful, nominal economic growth is higher than observed since the 2008 financial crisis on average, profit margins move slightly higher, and valuation multiples are also slightly higher than the recent historical average.