Market Recap

In the second quarter of 2025, global markets faced a complex mix of encouraging economic data, ongoing geopolitical uncertainty, and evolving global central bank policies. Nonetheless, the S&P 500 index posted a strong gain, reaching a new all-time high, and fixed-income markets were positive across most segments.

The S&P 500 (U.S. large-cap stocks) gained 10.94% in the second quarter, driven by continued earnings resilience in the technology and communication services sectors. Year to date, the index is up 6.2%. The Nasdaq posted a stronger 17.96% return for the quarter, lifted by optimism around AI-driven productivity and corporate investment in cloud infrastructure. U.S. small-cap stocks also moved higher in the three-month period, gaining 8.5% (Russell 2000).

Internationally, developed market performance was also strong gaining 11.78% (MSCI EAFE). Importantly, most of this return is due to currency effects, specifically a weaker U.S. dollar. (In local currency, returns were 4.8%.) Emerging markets rose 11.99% (MSCI EM) benefiting from improving sentiment around China’s fiscal stimulus and currency stabilization efforts. Geopolitical risks, including ongoing instability in Eastern Europe and the Middle East, remain potential catalysts for volatility.

Within fixed-income, our expectation has been that rates will remain volatile but without a clear direction, which played out in the second quarter. The 10-year Treasury yield started the quarter at 4.23% and ranged between 4.01% and 4.58% before ending the quarter at 4.24%. In the period, investment-grade core bonds ended the quarter up 1.21% (Bloomberg US Aggregate Bond). Lower quality high-yield bonds were up 3.57% (ICE BofA US High Yield) as investors’ appetite for risk .

Macroeconomic and Investment Outlook

At their mid-June meeting, the Federal Reserve (the “Fed”) held the federal funds rate steady at 4.25–4.50%, marking the fourth consecutive meeting without a change in interest rates. Chair Jerome Powell again emphasized a data dependent approach, citing risks from tariffs and global uncertainty, particularly inflation pressures from U.S. tariffs. The Fed also updated their summary of economic projections where the key takeaway was that the median forecast is still for two quarter-point interest rate cuts by the end of 2025. However, there was some division within the Fed, where seven of 19 officials now see no cuts this year, implying that they believe the economy is stable and interest rates are not too restrictive.

The Fed’s rate decisions are based on their dual mandate of stable prices and maximum employment. When it comes to inflation, Fed officials have acknowledged slower progress toward their 2% inflation target, citing wage growth and shelter costs as persistent headwinds. Markets now expect the first rate cut to occur late in the third quarter or early fourth quarter, which will be subject to future inflation and labor metrics.

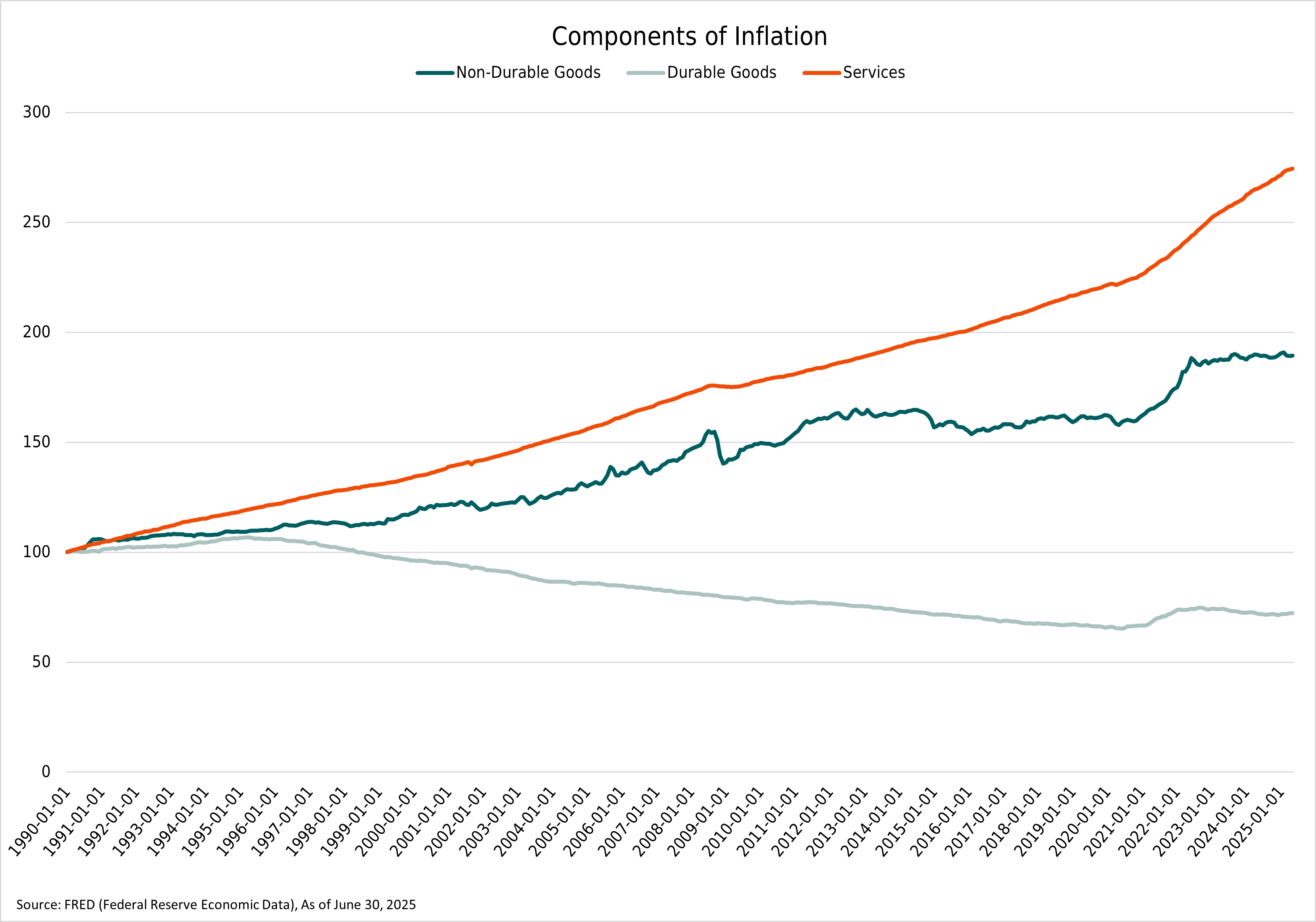

Our view is that inflation, from a structural perspective, remains under control. For example, the Consumer Price Index (CPI) ex-shelter, has been below the Fed’s 2% target in 19 of the past 24 months, underscoring the disinflationary trend in much of the economy. When breaking down the components of inflation (as shown in the chart below), the only area that has been showing inflation is services, specifically shelter. In contrast, both durable and nondurable goods have been flat to deflationary since 2022. While upcoming tariffs may temporarily push inflation higher, the Fed is likely to look through these shorter-term effects and focus on the underlying structural picture, which we think remains benign.

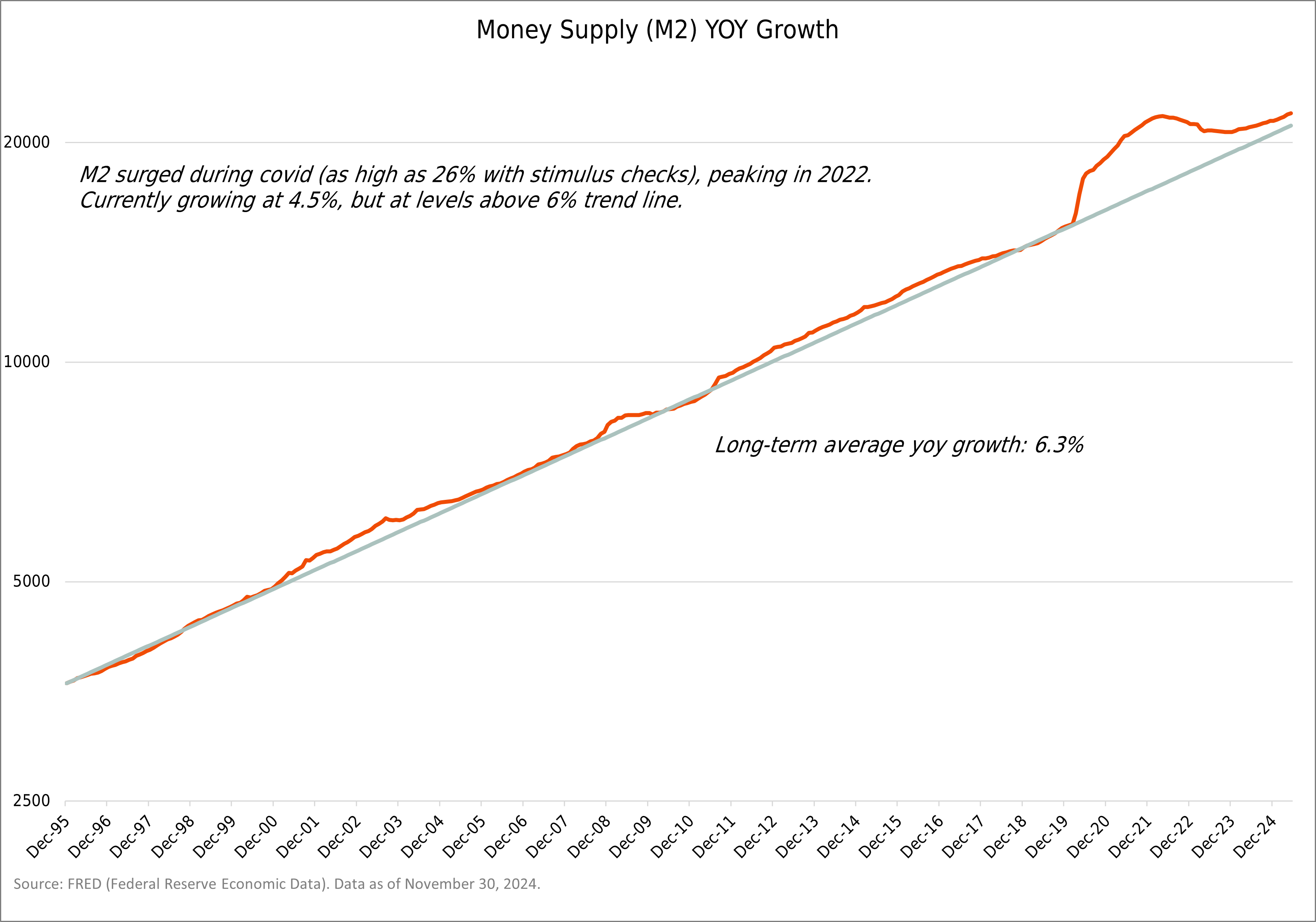

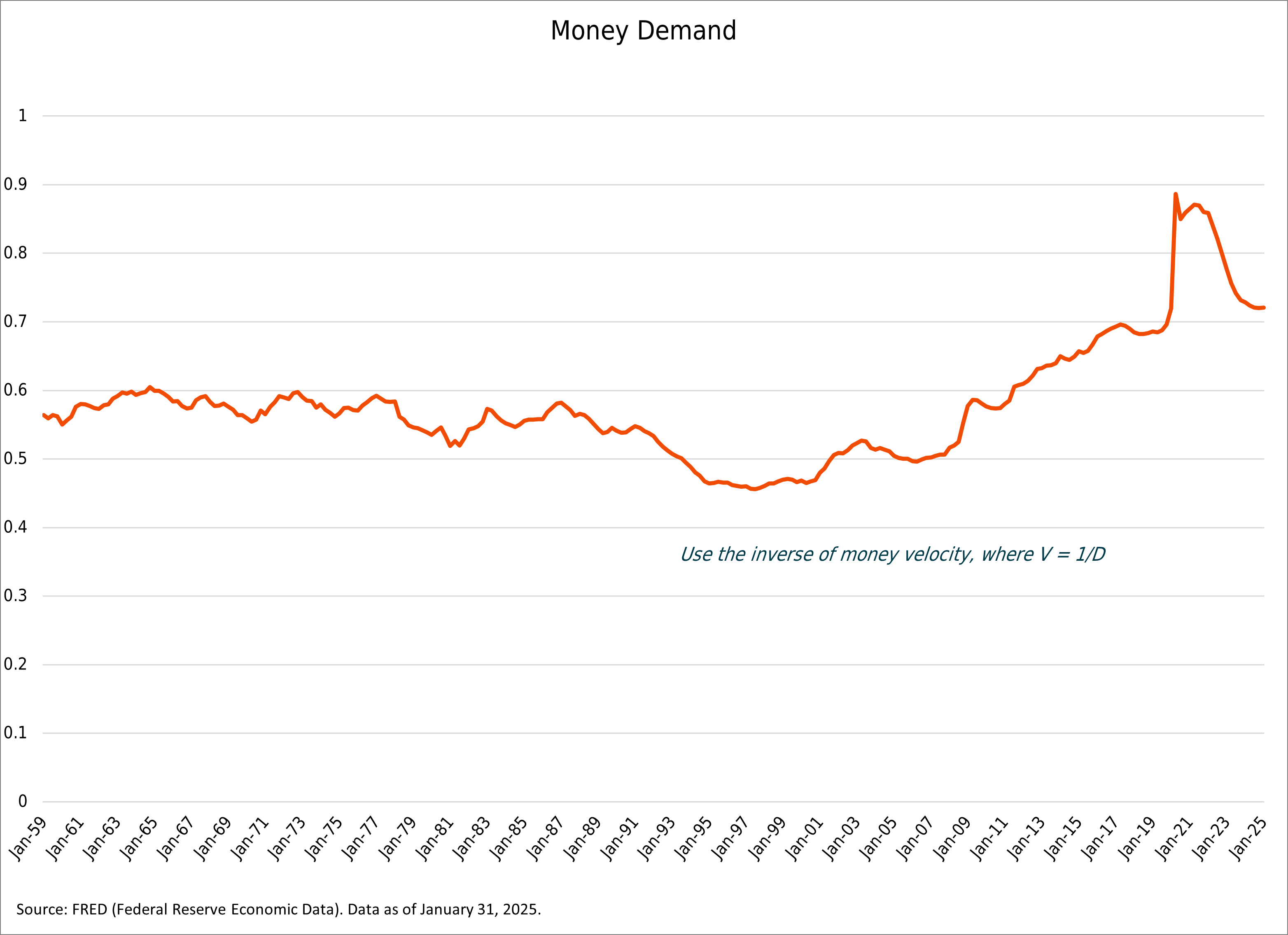

Two measures we use to assess our view on structural inflation are the balance of money supply and money demand. Here we use M2 as a barometer of money supply (tracking very liquid assets such as savings and checking accounts, money market funds, etc.), and the inverse of money velocity as a measure of money demand, or the desire to hold money rather than spend it, which depends on factors such as income levels, interest rates, and economic uncertainty.

When these supply and demand measures are roughly in balance, inflation is likely to be relatively steady. It’s when these measures are out of balance that you can expect more meaningful swings in inflation. A prime example was the government’s post-Covid fiscal policy, which pushed trillions of dollars into the economy. Despite a massive injection of stimulus into the economy, inflation initially remained steady. This is because the economy was essentially closed for business, and consumers could not spend. Therefore, the increase in money supply was matched by a proportional increase in money demand.

The chart below shows that from 1995 through 2019, M2 grew at just over 6% (annualized). This was a period with relatively stable (and low) inflation, which implies that money supply and demand were in balance. But in March 2020, you can see that M2 spiked from the stimulus, but it wasn’t until early 2021 that inflation started rising. Rising inflation was due to a collapse in money demand as the economy reopened in early 2021 and consumers rushed to spend their money, particularly on services such as travel. This sudden and dramatic imbalance resulted in an inflationary spike, with supply chain issues exacerbating the situation.

Our current view is that the structural forces that have historically driven inflation in the U.S., particularly the balance between money supply and money demand, are currently in equilibrium. These structural forces, which we sometimes refer to as the “gusts of wind” in the inflation landscape, tend to dictate the broader direction and persistence of inflation over time. Since the post-pandemic period of imbalance, both the supply of money and demand for money have normalized, contributing to the overall disinflationary trend we’ve seen across much of the economy.

At the same time, we recognize other forces do have an impact. These smaller, more transient forces, or “breezes” in this analogy, can still influence inflation in the near term. These may not overturn the broader trajectory, but they can introduce directional pressure. A current example is the tariffs, which we expect will exert upward pressure on goods prices. While unlikely to cause a sustained inflationary spike, these policy developments could complicate the near-term inflation picture and until now have reinforced the Fed’s cautious tone.

Another inflationary “breeze” we have been monitoring is shelter, which carries meaningful weight in the services segment of the economy. The way shelter inflation is measured in official data tends to lag reality by about 18 months and likely overstates current housing cost pressures. As more real-time housing data flows through, we expect this component of inflation to continue moderating, helping to push inflation lower. So, while we see the core inflation dynamics as fundamentally well-anchored, we continue to monitor these secondary influences for their potential to temporarily sway the path of prices and affect Fed policy decisions.

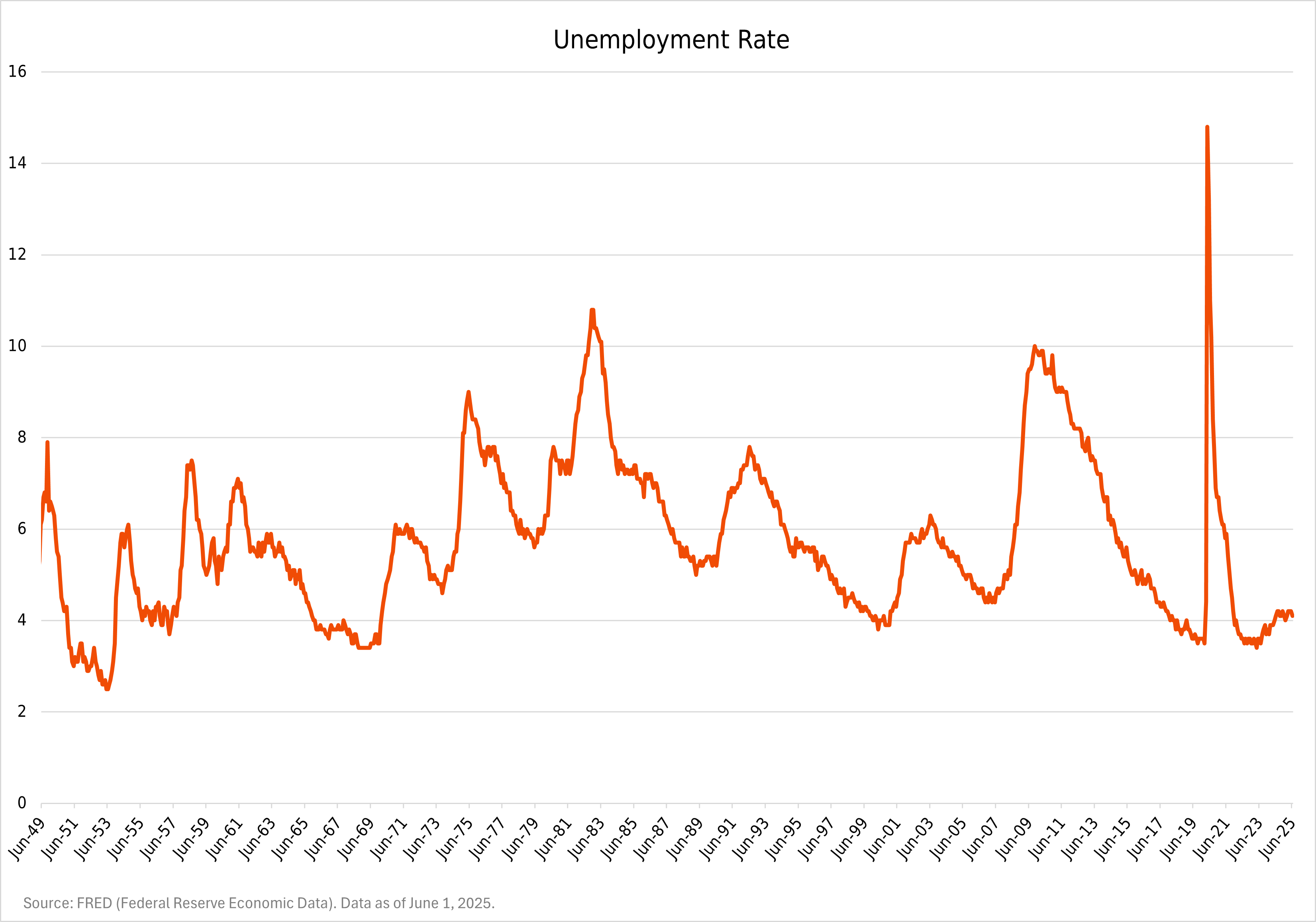

As for the labor market, it is showing signs of slowing and is not likely to improve meaningfully given the shift to more restrictive immigration policies.. Unemployment ticked up modestly to 4.1% in June, and job openings have declined across several sectors. Fed officials expect unemployment to rise to 4.5% this year (from 4%) and settle at 4.4% in 2027. Wage growth remains above pre-pandemic trends but has decelerated, which could provide relief for the Fed’s inflation mandate in the coming quarters.

Looking at economic growth, U.S. GDP growth in the second quarter is estimated to have reaccelerated to 2.5% annualized after contracting 0.2% in the first quarter. (This is according to the Atlanta Fed as of July 1, 2025.) The first quarter’s GDP decline was primarily due to a surge in imports ahead of the tariff announcement (imports are a subtraction in the GDP calculation). The Bloomberg consensus estimate for 2025 GDP growth is 1.4%. Consumer spending, though still positive, has recently shown some signs of fatigue as households continue to adjust to higher borrowing costs and tighter credit conditions.

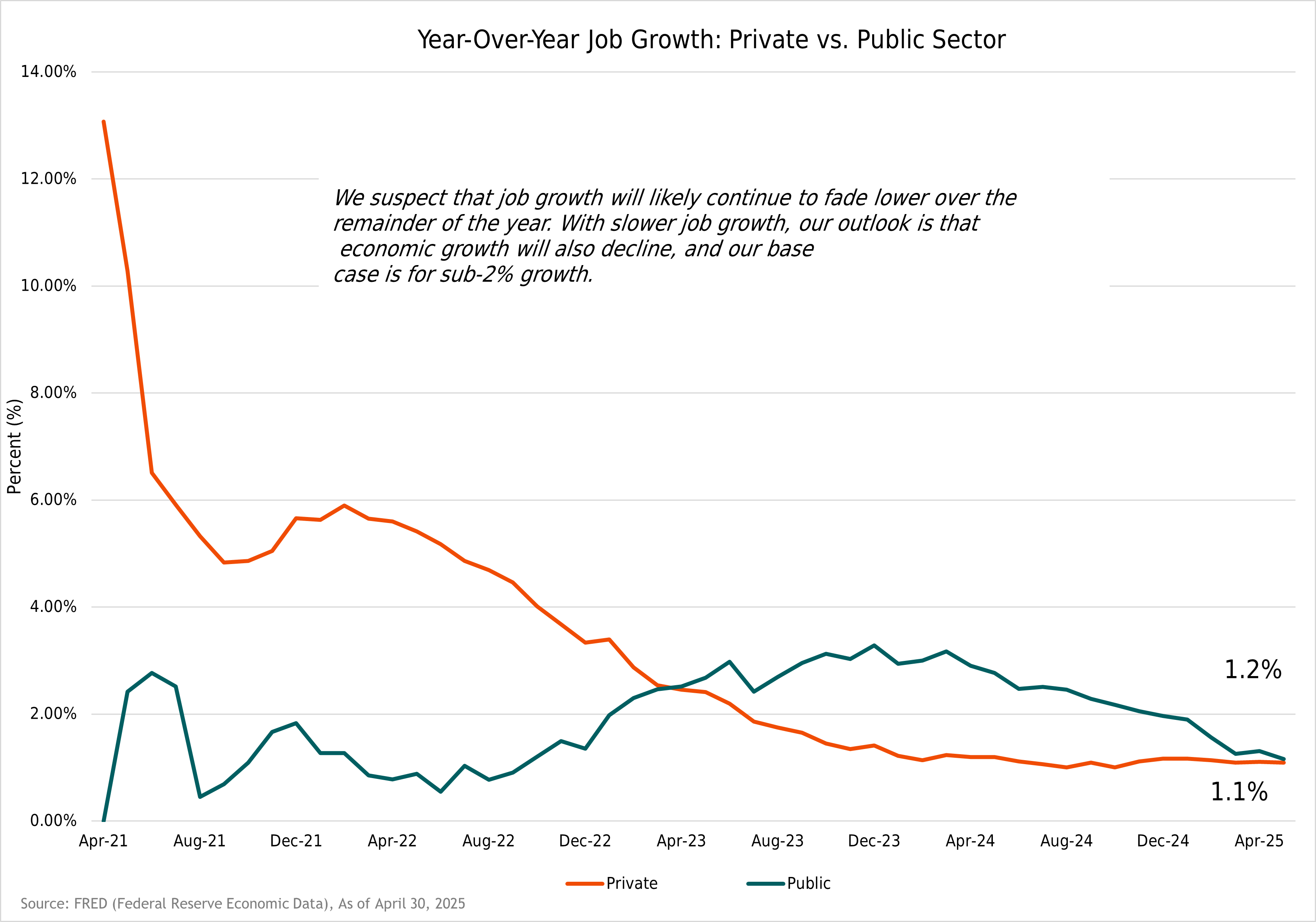

Job growth is one measure we look at when considering economic growth. As shown in the chart below, year-over-year job growth for both private and public segments have slowed to just over 1%. We think it’s possible job growth could slow from these levels, which would support only modest economic growth.

We expect the U.S. economy to slow in the near term but continue to believe it can avoid a meaningful downturn and ultimately regain momentum over time. On inflation, our view is that unless tariffs are significantly broadened or met with retaliatory measures, their overall impact on consumer prices will be limited over the next 12 to 18 months. Furthermore, some of the inflationary effect may be absorbed through corporate margins or offset by disinflation in other areas, particularly shelter, which we believe remains overstated in official data.

With core inflation continuing to trend toward the Fed’s 2% target (albeit slowly) and clearer emerging signs of economic and labor markets softening, we believe the Fed now has room to begin cutting interest rates. The timing and pace of those cuts remain uncertain, but in our view, the case for monetary easing has become increasingly compelling to support the slowing economy.

Global Equities

The second quarter started out with significant volatility with the tariff announcement on April 2nd. The punitive tariffs were meaningfully higher than investors had been expecting. This negative surprise sent equity markets sharply lower. The S&P 500 fell 4.8% and 6% on April 3rd and 4th, respectively. The sell-off continued until April 9th when a 90-day pause on all tariffs was announced, (as of July 7 the pause has been extended to August 1). Following the pause, the S&P 500 rallied 9.5% in a single day and continued to rally over 25%, recovering all the losses experienced since the market peaked in mid-February.

By the end of the quarter, the S&P 500 had reached its all-time high at 6,204, bringing its year-to-date return to 6.2% through June.

While most assets have seen their values recover, that hasn’t been the case for the U.S. dollar. The dollar continued to weaken throughout the quarter and has fallen over 10% on the year. The U.S. Dollar Index has fallen to levels last seen over three years ago. We have long written about the dollar and its importance to foreign equity returns relative to U.S. equities. Should the dollar continue to trend lower, this would continue to be a tailwind for foreign equity returns relative to domestic returns.

So far, the uncertainty and angst surrounding the tariffs has mainly impacted market sentiment and not fundamentals. First quarter earnings wrapped up with a strong showing, growing over 13% compared to a consensus forecast of mid-single digit growth at the start of earnings season. The bigger test will be over the next two quarters, which will start to incorporate the impacts from tariff.

Fixed-Income

U.S. Treasury yields moved modestly lower across most of the yield curve during the quarter, reflecting growing expectations that the Federal Reserve is approaching an inflection point in its policy stance. The 10-year yield declined approximately 20 basis points over the quarter, ending near 4.20%, while the 2-year yield fell slightly more, reflecting anticipation of rate cuts by year-end. The curve was slightly inverted at the end of June, a signal of shifting market sentiment toward a softer economic trajectory.

While we suspect economic growth will slow, this does not necessarily spell trouble for corporate bonds. A moderate slowdown can be supportive, as it eases inflation pressures and interest-rate volatility, both of which help maintain credit stability and investor demand.

While interest rates were volatile for most of the year with swift and meaningful moves, rate volatility has subsided a bit late in the second quarter. For example, the MOVE Index (a proxy for Treasury market volatility) declined meaningfully as economic data began to show more consistent signs of slowing inflation and moderate growth. The more stable macro backdrop contributed to a less reactive interest-rate market, even as Fed communications remained cautious.

Investment-grade and high-yield corporate bonds posted gains in the quarter, and spreads remained broadly resilient. Investment-grade spreads tightened modestly, supported by solid corporate fundamentals, low default activity, and ongoing demand for high-quality yield. High-yield spreads experienced some mild widening mid-quarter amid pockets of risk aversion but tightened by quarter-end, finishing largely unchanged. Overall, credit markets reflected a “soft landing” consensus, though with increasing focus on idiosyncratic risk and corporate refinancing needs heading into 2026.

Looking ahead, with our view that inflation is largely under control, particularly outside shelter-related services, and the economy showing signs of deceleration, the Fed appears to have the flexibility to begin cutting rates in the second half of the year. We expect the front end of the curve to remain most sensitive to shifting rate expectations, while long-end yields may be more anchored by growth and inflation dynamics. Credit markets are likely to remain stable in the near term but warrant more selectivity, particularly in lower-rated segments where refinancing risk and credit dispersion may rise.

Portfolio Positioning

Given the current macro backdrop for inflation, a slowing but resilient economy, and expectations for policy easing, we remain positioned with neutral strategic equity allocations across the U.S., developed international, and emerging markets. While U.S. equity valuations are undeniably elevated by historical standards, that alone does not imply an imminent correction as valuations have long proven to be poor timing tools.

In fixed-income, we continue to see opportunities to outperform the core bond benchmark. Rate volatility has subsided somewhat in the second quarter, and with the current backdrop we expect yields to remain rangebound between approximately 3.80% and 4.60% on the 10-year Treasury. We have been trading around these ranges, shortening duration last year when yields were in the upper 3% range and adding some duration back recently when rates were in the mid-4% range.

Overall, we remain underweight duration. This positioning reflects our view that attractive yield opportunities remain across credit (including high-quality and selective high-yield exposure) and securitized markets, allowing us to capture attractive income without overreaching for return and helping narrow the range of portfolio outcomes in an environment of still-evolving macro conditions.

Within alternative strategies we continue to own diversifying positions in “trend-following” managed futures across most portfolios. These positions have lagged this year amidst the sharp market reversals but remain a valuable diversifier.

Closing Thoughts

The second quarter’s equity rebound reflects growing investor optimism that a soft landing remains likely, with inflation easing and central banks, particularly the Fed, gaining room to cut rates. In the U.S., equity performance continues to be led by a narrow set of large-cap growth/technology stocks, though market breadth has improved modestly from last year.

Outside the U.S., valuation discounts for international stocks remain meaningful relative to the U.S., but currency dynamics and geopolitical uncertainty continue to present near-term risks. We see potential for select international exposures to outperform, particularly if the dollar continues to weaken alongside Fed policy shifts.

As we enter the second half of 2025, our outlook remains constructive but cautious. We believe markets will continue to be shaped by a tug of war between slowing economic growth and the prospect of rate cuts alongside further resolution to the tariff situation. We continue to think economic growth will slow but not collapse. Themes to watch in the remainder of the year will be Fed policy shifts, corporate earnings strength, and geopolitical risks.

As always, we remain committed to helping you navigate this dynamic environment with a disciplined, long-term approach.