Originally published November 29, 2022 – Updated as of December 2, 2025

As the year-end fast approaches, ‘tis the season for giving – and for those who donate to charity, choosing the right strategies can impact how much goes to the charitable organizations versus Uncle Sam. The best giving strategy depends on each individual’s circumstances, so we will cover only the main points in this post – if you want more color on any of these areas, or how you can use them, please don’t hesitate to reach out to your advisor.

Donating Appreciated Securities

The go-to advice for optimizing the dollars available for charity versus those spent on taxes is through directly donating assets that have gone up in value (and have been held for more than one year) rather than gifting cash. Because donating securities does not trigger capital gains for either the giver or the charitable recipient, the effect can be to eliminate future capital-gains tax liability for the giver. And if you still want to own the amount gifted of a particular security, you can simply repurchase shares with the less tax efficient cash you would have otherwise donated – leaving you in a similar investment position, but with a lower tax liability. Appreciated securities can be donated directly to a charity(ies) or can be contributed to a “donor advised fund” account.

Donor-advised funds (DAFs) – For those expecting to make ongoing charitable contributions, a donor-advised fund is an attractive option. In effect it creates a personal “gift fund” in the form of a giving account, whose assets are irrevocably committed to be granted to qualified charities and with the donor receiving a tax deduction in the year that assets are gifted into the DAF. One of the benefits of using these charitable accounts is that the amounts and eventual timing for grants to charities are at your discretion. You also can invest the account’s assets, and any tax-free returns that may be generated increase the dollars available to grant.

Qualified Charitable Distributions (QCDs) from IRAs

These are donations to charity made directly from an IRA account whose owner who is at least age 70 ½. The total amount that can be given as QCDs each year is subject to an IRS-set annual dollar limit (indexed for inflation; for 2025 the limit is $108,000 per individual), and those QCDs will not be subject to income tax, unlike regular IRA withdrawals. The result is that the amount withdrawn and donated directly from the IRA is excluded from taxable income, providing a potential tax benefit.

Further, if the IRA owner has reached the age at which they are subject to annual required minimum distributions (RMDs) under current IRS rules (currently age 73 for most taxpayers), the amount donated as a QCD can be used to help satisfy their RMD. And if these donations are made during the period before RMDs begin, the reduced IRA balance in turn lowers the amount of future RMDs.

A few important points about QCDs:

- IRA owners over age 70 ½ are eligible to request QCDs

- Donations must be made directly to the charity(ies) from the IRA custodian

- The total of all QCDs in a tax year can not exceed the annual limit for QCDs (for 2025, $108,000 per individual; this limit is indexed for inflation)

- Although QCDs will not be taxable to the IRA owner, they are still shown the same as other taxable distributions on the tax Form 1099-R, so you and your accountant must be sure to report the QCD amounts as non-taxable

- The tax benefit exists regardless of whether your itemized deductions exceed the standard deduction – though if they do exceed the standard deduction it may make sense to consider donating appreciated securities, if that’s an option

Tax rules, including age thresholds and dollar limits, are subject to change and can vary based on your situation. Be sure to confirm current IRS rules and consult your tax advisor before implementing these strategies.

Your advisor can work with you to evaluate the available options, and help coordinate any communication needed with your tax advisor.

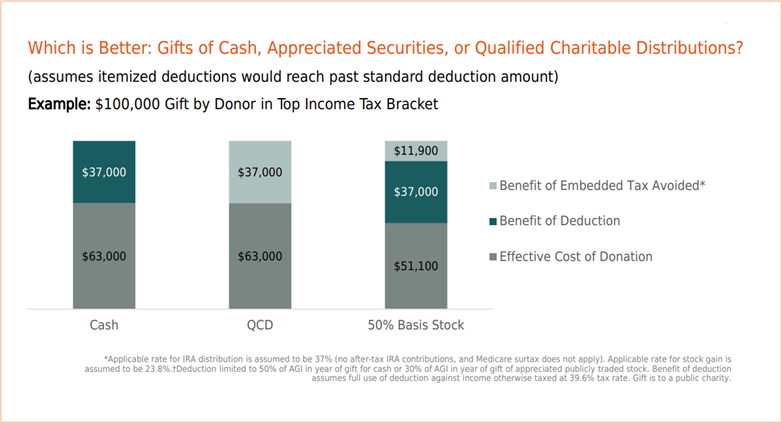

Both donating appreciated securities and QCDs are attractive strategies; which is best depends on individual circumstances. The chart that follows shows the tax benefits of deductions, avoided taxes, and effective donations for both QCDs and donating appreciated stock versus a baseline of donating cash.

Illustration is hypothetical and for illustrative purposes only. Actual tax outcomes will vary based on individual circumstances and current tax law.

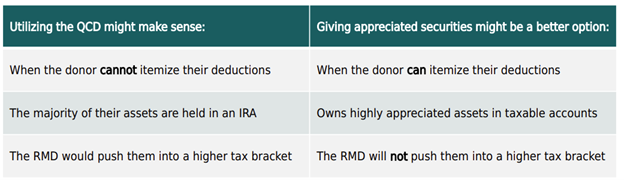

In the above example the nod goes to the 50% basis stock, by virtue of the avoidance of capital gains tax, lowering the effective cost of the donation. Here is another graphic that lays out which option might make more sense depending on your tax situation:

Illustration is hypothetical and for illustrative purposes only. Actual tax outcomes will vary based on individual circumstances and current tax law.

These rules of thumb are helpful in framing the issue, but they do not take into account other possible factors, so we encourage you to talk to your advisor, who will be happy to provide guidance.

Developing a Philanthropic Mindset in Future Generations

Since the holiday season is a time focused on both family and helping others, we will conclude by sharing some ideas for our clients looking to connect with their family and introduce ideas around a meaningful giving strategy.

Including younger family members in your philanthropic activities is a way to pass on personal values, share experiences, establish family traditions and promote a spirit of community. Further, involving family members in philanthropy may be an important part of your overall wealth transfer plan.

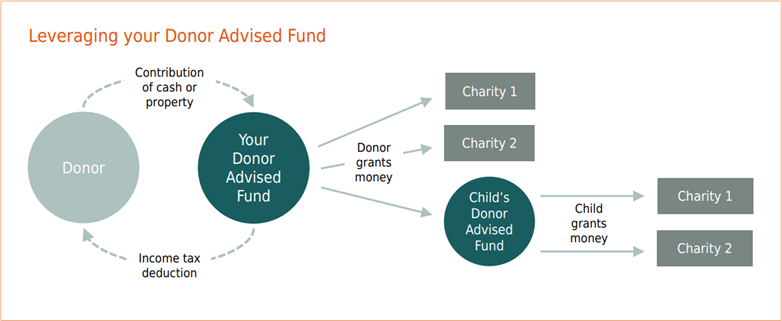

There are ways that you can leverage your donor advised fund to engage your next generation in charitable giving. For example, some of our clients have chosen to create a “family” charitable account where family members come together to discuss nonprofit organizations they’d like to support each year. Some even allocate a set amount for each family member and invite them to identify an organization to whom they want to donate. The conversations about philanthropic interests can also serve to create bonding and comradery among family members.

A step further is to “gift” or create a DAF account for your next generation, which you can do by granting funds directly from your existing account to a new DAF in their name. We’ve shown this idea in the illustration that follows.

Illustration is hypothetical and for illustrative purposes only. Actual tax outcomes will vary based on individual circumstances and current tax law.

These are just a few of the ways that you can engage with your family, but there are sure to be more. If you have found effective ways of engaging your family members in a mindset of giving, we’d love to hear about them and will share it with others who may find it helpful.

As always, we are here to help. Don’t hesitate to reach out with questions – your advisor is well-versed in charitable giving strategies and can help you take into account individual circumstances that may guide decisions.

Happy holidays and best wishes to all for a happy and prosperous 2023!