Actions to Take in Uncertain Times

During a volatile market environment like we find ourselves in today, or the steep market pullback at the onset of the pandemic in 2020, we know many investors feel a powerful drive to take some kind of action in response. Most commonly when markets are down sharply the action desired is to sell stocks as a way to reduce risk. While taking action creates a sense of control that can make people feel better in the moment, most often in these situations it’s exactly the wrong thing to do at that time. The iMGP Chief Investment Officer, Jeremy DeGroot said it well in an investment commentary:

As a long-term investor, trying to time market tops and bottoms is a fool’s errand. The evidence is overwhelming that most investors diminish their long-term returns trying to do so. They are more likely to chase the market up and down, and get whipsawed, buying high and selling low.

As we wrote back in 2020, market timing, while tempting, involves getting two nearly impossible decisions right: when to sell and when to get back in. Below is some updated information about the impact of making reactionary investment decisions.

Missing the Best Days

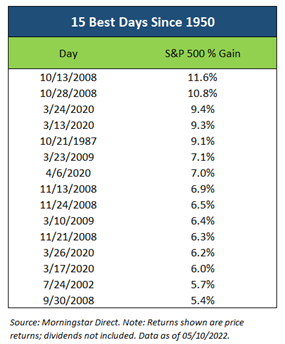

This table shows the 15 best days for the S&P 500. Surprisingly, all of them occurred within bear markets, not bull markets as you might expect. That is, the big upturns in the stock market can happen during times when it’s hardest to remain invested or tempting to get out of the market and wait for better days. Looking at these dates, you’ll find the who’s who of dark times for the stock market: the 2008 financial crisis, the dot-com crash, the Black Monday crash of 1987, and the pandemic-driven market decline in 2020.

By trying to miss the worst days, investors are very likely to miss the best days. In studies of behavioral finance, “recency bias” suggests that someone’s most recent experience has the greatest influence on their decisions. As such, investors tend to sell after a meaningful market selloff and buy after a market rally.

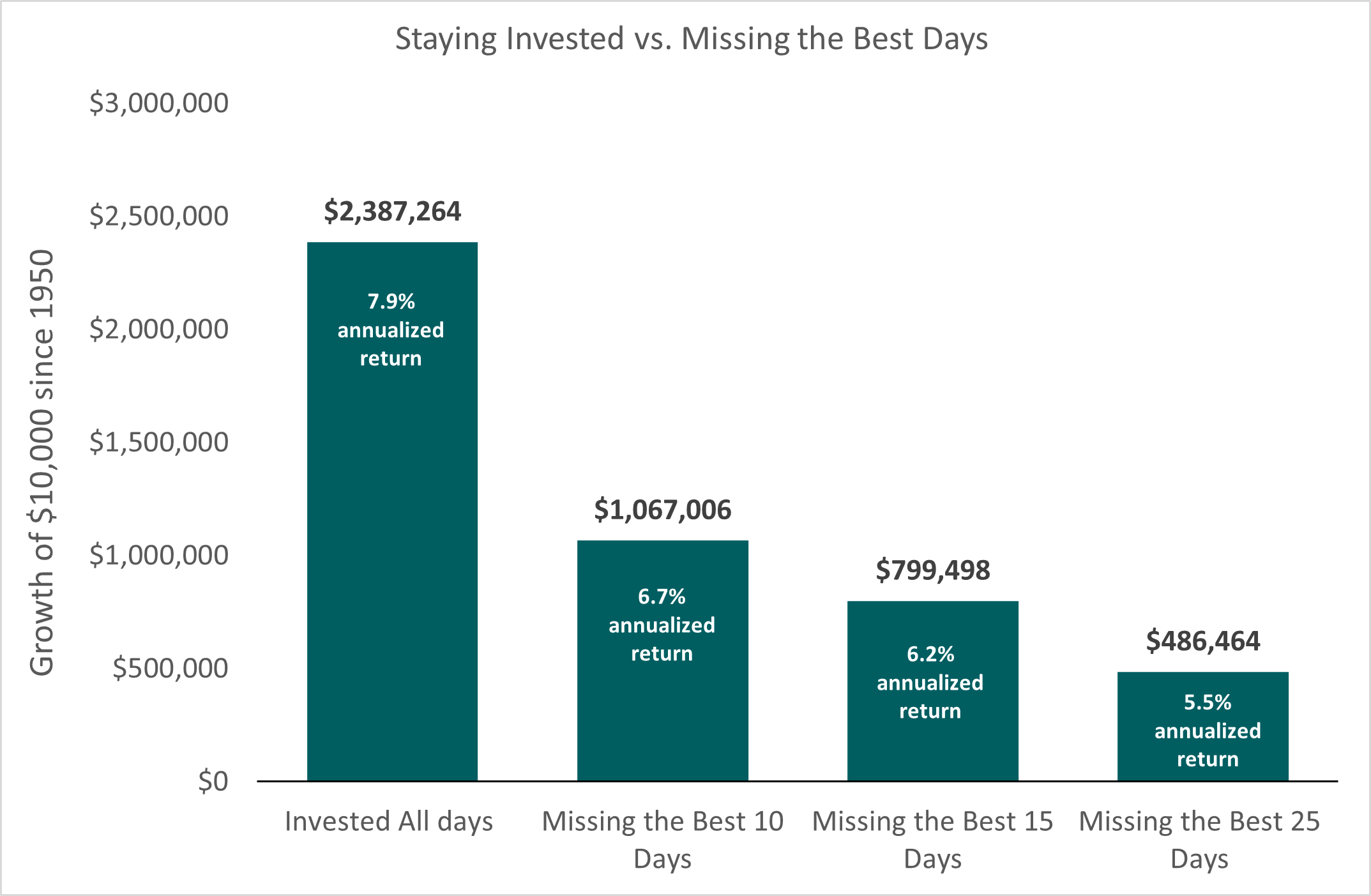

Missing just the 10 best days (out of more than 17,500 trading days since 1950) has a huge long-term effect on a portfolio. For example, an investor who invested $10,000 in the S&P 500 in 1950 would have gained 7.9% annualized and finished with a portfolio value of more than $2.38 million (as of 5/10/2022) if they had remained fully invested (not including dividends). The final portfolio value for an investor that missed the 10 best days is well below half that amount at roughly $1.07 million.

Source: Morningstar Direct: Price returns, excludes dividends. Data as of 5/10/2022.

Now it is unlikely an investor will only miss the best days if they sell in an attempt to time the market. They might also be able to miss some of the historically bad days. However, the cautionary tale of attempting to time the market is the same: There can be a huge cost to pay if the market swings to the upside while you’re on the sidelines. It would take exceptional timing skills to get in and out of the market perfectly, particularly since it needs to be done in short order given the market’s best and worst days tend to cluster close to one another. Staying the course is the best plan of action during periods of severe market stress. There is an old investing adage: “Time in the market beats timing the market.”

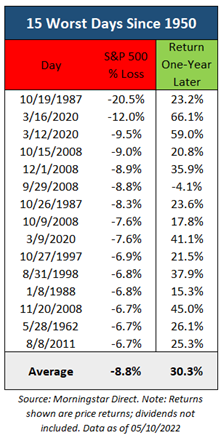

Owning stocks on historically bad days can be unsettling, but outcomes over the next year tend to be favorable. Investment industry giant BlackRock recently published a table showing one-year returns following the worst days for the S&P 500. The average one-year return after a historically bad day has been 30.3%. And there has only been one instance of a negative return.

Remain Invested, Stay Disciplined, and Seek Actionable Opportunities

This period of global unrest and economic uncertainty is still unfolding, and the drive to act can be difficult to resist. .In our role as wealth advisor to our clients, we take seriously our responsibility to help guide thoughtful decision making and wise action. Today more than ever, we want to focus on what we can control and not let ourselves be distracted by things we can’t. In discussions with clients we have found there are a number of positive steps that we can take together during this time. Below are several of the more common actions we are recommending:

- Keep a long-term perspective. One of the important benefits of working with us as your advisor is that we can help you manage your financial situation in a holistic way, which will enable you to stay true to your long-term investment strategy guidelines and discipline. This is true both for your existing investments as well as any new investments you plan to make over time. In that process we can help you resist the urge to sell out of equities during a downturn, only to then have to try to decide when to eventually get back in. As the charts above show, rebounds can happen quickly and the cost of missing them is significant over time. Instead, our goal is to help you stay invested, at a reasonable allocation level, which is the only way to ensure participating in the recovery in prices that history shows is critical to achieving long-term success. What’s more, we can prudently and incrementally add to stocks when their prices become more attractive and their future expected returns are better. With this strategy we can potentially take advantage of a volatile market environment and by adding to investments at prices likely to generate far better long-term returns that what was possible before this period began. This is one of the best ways for us to support you reaching your financial goals in the years to come.

- Confirm an appropriate “emergency fund”. One of the best strategies to help you sleep at night, even during market volatility, is to ensure the funds you need for spending in the near future are not at the mercy of short-term market movements. We work with clients to make sure they have an appropriate amount of cash or low-volatility investments set aside to fund either spending needs or just as an emergency fund—keeping this money steady when the near future is unknown. This is something we can revisit with you if it is an area of concern.

- Revisit financial planning and/or cash flow projections. By reviewing how your resources will support cash flow needs into the future, we can help ensure that your spending should be sustainable. And if making changes to expenses in the near term would be advantageous, that could be a positive step to take during a difficult time. Reviewing scenarios for how the future may play out can be very helpful in creating the appropriate context for making decisions today.

- Use market declines as an opportunity to harvest tax losses. A downturn in prices isn’t what we hope for when investing. But one way to make lemonade out of those lemons is to sell securities that are down from their purchase price. By “harvesting” those realized losses they can be used to offset taxable realized gains. This tax-saving strategy can be helpful today and possibly for many years into the future, since realized capital losses can be carried forward on your tax return. As we harvest losses, the proceeds from those sales are used to purchase investments in a similar category, so your portfolio allocation and opportunity to catch an upswing stay intact.

- Consider a Roth IRA conversion. Roth conversions offer the opportunity to transition investments from a traditional tax-deferred IRA account to a Roth IRA, where they will benefit from tax-free growth going forward. The conversion will be taxable, but a market downturn could be a good time to make this transition with assets that have fallen in price, as their subsequent growth when the market recovers will be in the tax-free Roth IRA.

- Take breaks from the 24/7 news cycle. We encourage you to take time away from the news and daily updates. The constant news feed is focused on getting attention and benefits advertisers, not investors. It can be overwhelming to the viewer, and that can lead to unnecessary stress and anxiety. It’s important to stay both physically and mentally healthy so you can make the best decisions for your overall benefit.

If you would like to review any of these or other actions that could benefit your situation, please do not hesitate to reach out to your Litman Gregory advisor for a more thorough and personal discussion.

—Litman Gregory Investment Team (5/12/22)